Let us begin with a short explanation of what opening balance is: The opening balance is the amount of funds that are bought forward from the end of one accounting period to the beginning of a new accounting period. In a firm’s account, the first entry done is of the opening balance. It can either hRead more

Let us begin with a short explanation of what opening balance is:

The opening balance is the amount of funds that are bought forward from the end of one accounting period to the beginning of a new accounting period.

In a firm’s account, the first entry done is of the opening balance. It can either have a debit balance or a credit balance depending upon whether the firm has a negative or positive balance.

Opening balance of a ledger

Opening balance is the first entry of the ledger account at the beginning of an accounting period.

In the case of a newly started business, there will be no closing balances and as such there will be no balances to be carried forward. In such a case, the investment and capital of the business will be entered as an opening balance for the current accounting period.

So the first and foremost part is to identify on which side of the ledger i.e. the debit side or the credit side the opening balance is to be entered.

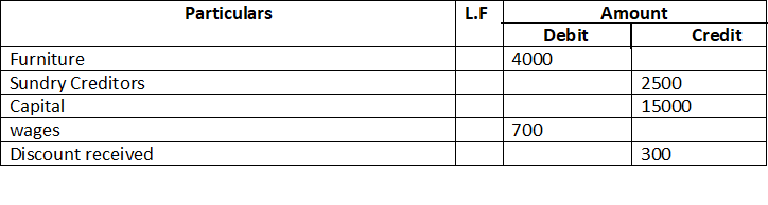

For Example, A trial balance is given which represents the debit and credit balances, accordingly, I will prepare different ledger accounts to make it simpler.

The trial balance shows the opening balance of various accounts. Now posting them in ledger accounts.

The trial balance shows the opening balance of various accounts. Now posting them in ledger accounts.

As the Furniture is an Asset account, the opening balance will be on the debit side of the ledger account.

As Sundry creditor is a credit account, we put the opening balance on the credit side.

As the Capital is a credit account, we put the opening balance on the credit side.

As Wages is a debit account, we put the opening balance on the debit side.

As the Discount received is a credit account, we put the opening balance on the credit side.

Exception

Drawing Account.

Drawing account is an exception to this topic. It is considered a contra account to the owner’s capital account because it reduces the value of the owner’s equity. Drawings, therefore, have no opening balance.

Contra Entry.

Contra entry involves transactions of cash and bank. Any entry which involves both the cash and bank is contra entry.

For example, we deposit cash 5000 into the bank.

Accounting entry for this transaction would be

In this case, the ledger entry would be

As the bank account has a debit balance, the opening balance would come on the debit side.

As the cash account has a credit balance, the opening balance would come on the credit side.

Alternatively, If we withdraw cash 5000 from the bank.

Accounting entry would be

In this case, the ledger entry would be

As the Cash account has a debit balance, the opening balance would come on the debit side.

As the Bank account has a credit balance, the opening balance would come on the credit side.

See less

A statutory reserve is any reserve that has to be maintained by an Act or law. When it comes to insurance, a statutory reserve is a reserve that an insurance company is legally bound to maintain to ensure that the company is able to meet its policy obligations. In India, as per the Banking RegulatioRead more

A statutory reserve is any reserve that has to be maintained by an Act or law. When it comes to insurance, a statutory reserve is a reserve that an insurance company is legally bound to maintain to ensure that the company is able to meet its policy obligations. In India, as per the Banking Regulations Act, every banking company has to maintain at least 25% of its net profits as statutory reserves.

The companies are required to maintain such reserves to guarantee the availability of cash when it is required by the customer. Common examples of statutory reserves are Cash reserve ratio (CSR), Statutory Liquidity Ratio (SLR).

Treatment

Method

Rule-Based Approach – The company calculates the amount required by using standard formulas. However, since they are pre-determined formulas, it does not cover all risk determining factors.

Principle-based approach – This method is used to protect customers and ensure that the company stays solvent. They hold a higher amount of reserves than required after predicting all possible risks.

Statutory reserves are different from general reserves as general reserves are maintained voluntarily by the company. A company that does not follow statutory requirements will face financial penalties. These reserves are mostly maintained in the form of cash.

Maintenance of reserves gives confidence to investors that their money is secure. However, funds from these reserves can be used only for specific purposes. They should also maintain such reserves whether or not they earn profits.

See less