Statutory Liquidity ratio is the minimum percentage of reserves of liquid assets that the commercial bank should maintain. These liquid assets are in the form of gold, cash, and other securities. These reserves are kept with the bank itself and not with the Reserve Bank of India. The bank holds variRead more

Statutory Liquidity ratio is the minimum percentage of reserves of liquid assets that the commercial bank should maintain. These liquid assets are in the form of gold, cash, and other securities. These reserves are kept with the bank itself and not with the Reserve Bank of India.

The bank holds various demand and time deposits of the public, the total of which is called Net Demand and Time Liabilities (NDTL). This includes demand deposits that have to be paid on demand. Various other deposits like time deposits, fixed deposits, demand drafts, etc. are also included.

Every bank must keep a portion of its NDTL in the form of cash, gold, or other liquid assets. Therefore, the Statutory Liquidity Ratio is the ratio of these liquid assets to the total demand and time liabilities. The authority to determine the ratio lies with the RBI, who can increase it to the extent of 40%.

FORMULA

PURPOSE OF SLR

RBI controls the flow of cash in the economy by means of monetary policy measures through financial instruments like Statutory Liquidity Ratio. At the time of inflation, RBI increases SLR to reduce the flow of cash whereas, at the time of deflation, they reduce SLR to increase the flow of cash. Maintaining SLR also helps ensure the solvency of the commercial banks.

If the banks do not maintain the necessary level of SLR, they would be liable to pay a penalty to RBI at 3% per annum above the bank rate, on the shortfall amount of that day.

See less

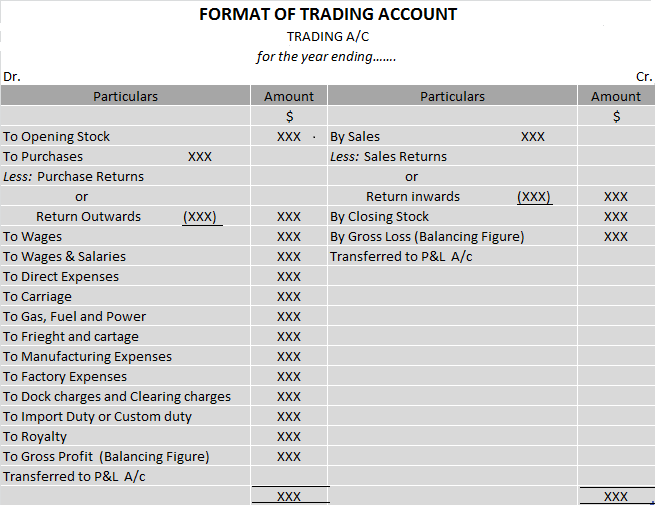

The profit and loss appropriation account is an account created in addition to the Trading & Profit and loss account in the case of partnership firms. It is a nominal account. The net profit or loss from the Profit and loss account is transferred to the Capital A/c when we do the accounting of sRead more

The profit and loss appropriation account is an account created in addition to the Trading & Profit and loss account in the case of partnership firms. It is a nominal account.

The net profit or loss from the Profit and loss account is transferred to the Capital A/c when we do the accounting of sole proprietors.

But, while doing the accounting of partnership, there is a need to appropriate this profit or loss as there are two or more partners’ capital accounts. So, for this purpose, the Profit and loss appropriation account is created.

The net profit or loss is appropriated among the partner’s capital after adjustment the items like partner’s salary, commission, interest on capital, interest on drawing etc. It consists of items related to the partner’s claim.

The format of the profit and loss appropriation account is as below:

Let solve a problem to sharpen our concept:

A and B are partners in firm sharing profits and losses in the ratio of 4:1. On 1st January 2019, their capitals were ₹ 20,000 and ₹ 10,000 respectively. The partnership deed specifies the following:

Prepare Profit and loss appropriation account for the year ending 31st December 2019.

Solution:

See less