Interest on capital Interest on capital is interest payable to the owner/partners for providing a firm with the required capital to commence the business. Normally, it is charged for a full year on the balance of capital at the beginning of the year unless some fresh capital is introduced during theRead more

Interest on capital

Interest on capital is interest payable to the owner/partners for providing a firm with the required capital to commence the business. Normally, it is charged for a full year on the balance of capital at the beginning of the year unless some fresh capital is introduced during the year.

When the business firm faces a loss, the interest on capital will not be provided. It is permitted only when the business earns a profit. Such payment of interest is generally observed in partnership firms. It is provided before the division of profits among the partners in a partnership firm.

If an owner or partner introduces additional capital to the business then, it is also taken into account for providing interest on capital.

Interest on capital in the accounting equations

Interest on capital is an expense from a business point of view, as it is payable to the owner and is not paid in cash. Being an income from the owner’s point of view, it is added to his capital account. And being a business expense from the business point of view, it is therefore deducted from the capital.

Hence, it further doesn’t create any change in the accounting equation mathematically but it’s mandatory to be shown as it plays a vital role in the profit and loss a/c and even helps the business save tax.

Example

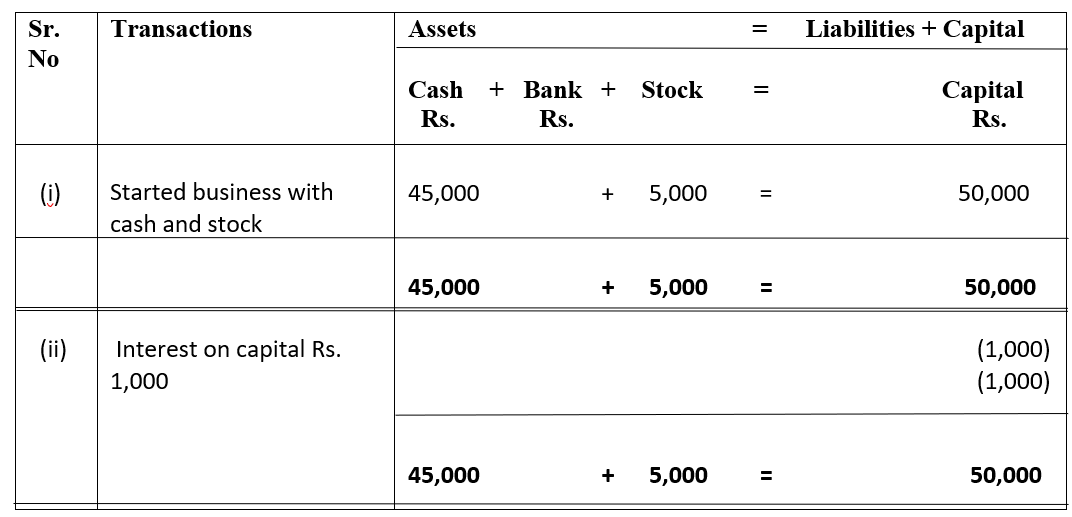

Z started a business with cash and stock of ₹45,000 and ₹5,000 respectively. Further, he received interest on capital of ₹1,000. The accounting equation for the following transactions will be as follows:

Accounting Equation

See less

The term set off in English means to offset something against something else. It thereby refers to reducing the value of an item. In accounting terms, when a debtor can reduce the amount owed to a creditor by cancelling the amount owed by the creditor to the debtor, it is termed as set off. It is coRead more

The term set off in English means to offset something against something else. It thereby refers to reducing the value of an item. In accounting terms, when a debtor can reduce the amount owed to a creditor by cancelling the amount owed by the creditor to the debtor, it is termed as set off.

It is commonly used by banks where they seize the amount in a customer’s account to set off the amount of loan unpaid by the customer.

Types

There are various types of set-offs as given below:

Example

Let’s say Divya owes Rs 20,000 to Sherin for the purchase of goods. But, Sherin owed Rs 6,000 to Divya already for use of her Machinery. Therefore, the amount of 6,000 can be set off against the 20,000 owed to Sherin and hence Divya would effectively owe Sherin Rs 14,000.

This helps in reducing the number of transactions and unnecessary flow of cash.

See less