Working Capital is the capital used in the daily operations of the business. It is calculated as the difference between current assets and current liabilities. Gross working capital means current assets and net working capital means the difference between current assets and current liabilities. WorkRead more

Working Capital is the capital used in the daily operations of the business. It is calculated as the difference between current assets and current liabilities. Gross working capital means current assets and net working capital means the difference between current assets and current liabilities.

Working Capital indicates the short-term liquidity of its business. It means the ability of a company to meet its daily requirements through short-term financing.

Working Capital can be;

- Positive

- Zero, or

- Negative

Positive or negative working capital follows a simple rule of math. If current assets are more than current liabilities, working capital is positive and if current assets are less than current liabilities, working capital is negative. When current assets are equal to current liabilities, working capital is zero.

Negative working capital for a short period means that the company has made a big payment to its vendors, or a significant increase in the creditor’s account because of credit purchases.

However, if working capital is negative for a longer period it indicates that the company is struggling with its operating requirements or that it has to finance its daily operations through long-term borrowings.

The current ratio for a company is calculated as:

Current Assets divided by Current Liabilities.

Working Capital and Current Ratio are interrelated. If the Current Ratio is more than 1, it means current assets exceed current liabilities and Working Capital is positive. However, if the Current Ratio is less than 1, it means current liabilities exceed current assets and Working Capital is negative.

For example-

If Current Assets are Rs 50,000 and Current Liabilities are Rs 70,000 then

Working Capital= Current Assets – Current Liabilities

WC = Rs 70,000 – Rs 50,000

WC = Rs. 20,000

Current Ratio = Current Assets / Current Liabilities

CR = Rs.50,000/ Rs. 70,000

CR = 0.71< 1

See less

The Income Tax 1961 does not provide any rate of depreciation specifically for cameras. But we can consider camera within the block of ‘Computer including software’ for which the rate of depreciation is 40% at WDV method. It is a general practice for non-corporates to charge depreciation at rates slRead more

The Income Tax 1961 does not provide any rate of depreciation specifically for cameras. But we can consider camera within the block of ‘Computer including software’ for which the rate of depreciation is 40% at WDV method.

It is a general practice for non-corporates to charge depreciation at rates slightly lower than the rate provided by the Income Tax Act, 1961. But one cannot charge depreciation more than it.

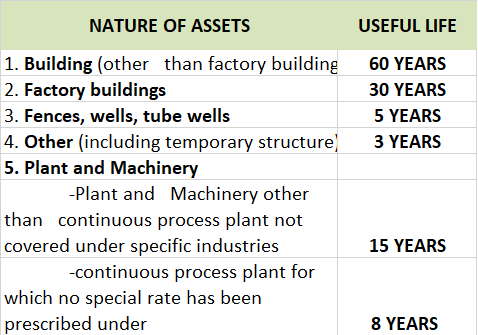

In the case of corporate, the rates for charging depreciation are provided by the Companies Act 2013, which is

Let’s take an example:

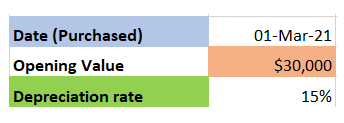

Mr X is a jewellery shop owner and has installed CCTV cameras on 1st April 2021, costing ₹ 40,000 at various points in his shop to ensure safety and security. Keeping in mind the Income-tax rates, his accountant decided to charge depreciation @ 30% p.a. on the CCTV cameras.

Following is the journal entry:

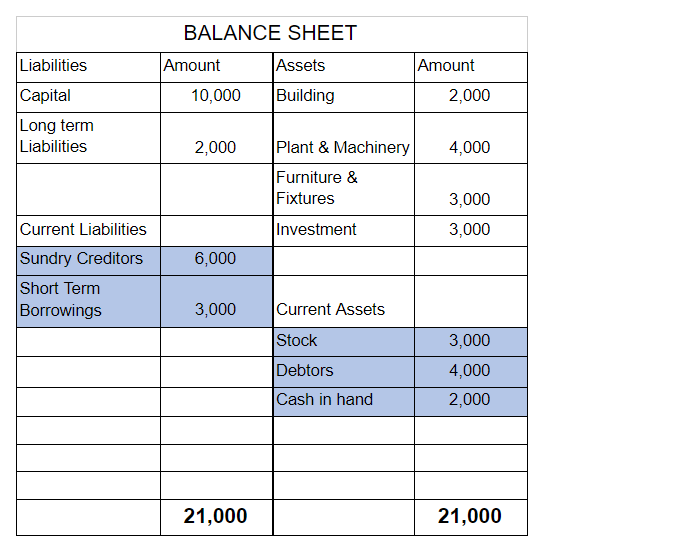

The balance sheet will look like this:

See less