Depreciation is an accounting method that is used to write off the cost of an asset. The company must record depreciation in the profit and loss account. It is done so that the cost of an asset can be realised over the years rather than one single year. Furniture is an important asset for a businessRead more

Depreciation is an accounting method that is used to write off the cost of an asset. The company must record depreciation in the profit and loss account. It is done so that the cost of an asset can be realised over the years rather than one single year.

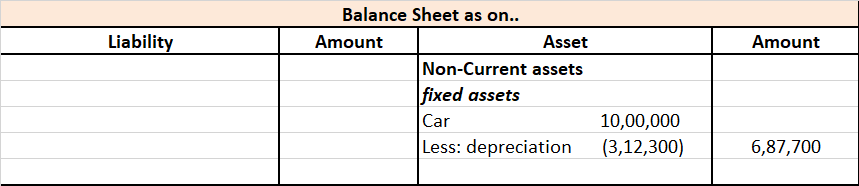

Furniture is an important asset for a business. As per the Income Tax Act, the rate of depreciation for furniture and fittings is 10%. However, for accounting purposes, the company is free to set its own rate.

JOURNAL ENTRY

Journal entry for depreciation of furniture is:

Here, depreciation is debited since it is an expense and as per the rules of accounting, “increase in expenses are debited”. Furniture is credited because a “ decrease in assets is credited”, and the value of furniture is reducing.

TYPES OF DEPRECIATION

Furniture can be depreciated in any of the following ways:

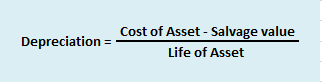

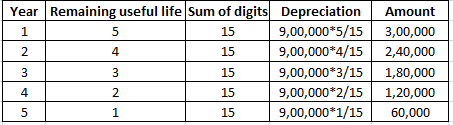

- Straight-Line Method – It is calculated by finding the difference between the cost of the asset and its expected salvage value, and the result is divided by the number of years the asset is expected to be used.

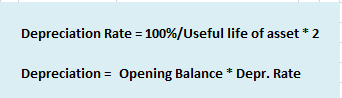

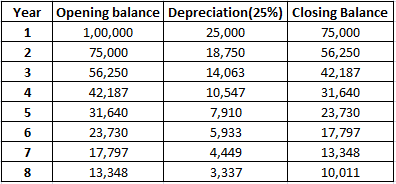

- Diminishing Value Method – It is calculated by charging a fixed percentage on the book value of the asset. Since the book value keeps on reducing, it is called the diminishing value method.

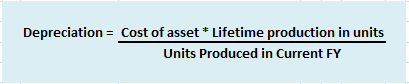

- Units of Production

For accounting purposes, the two many methods used for depreciating furniture is the straight-line method and the diminishing value method. However, for tax purposes, they are combined into a block of furniture, where the purchase of new furniture is added and the sale of furniture is subtracted and the resulting amount is depreciated by 10% based on the written downvalue method.

EXAMPLE

If a company buys furniture worth Rs 30,000 and charges depreciation of 10%, then by straight-line method, Rs 3,000 would be depreciated every year for 10 years.

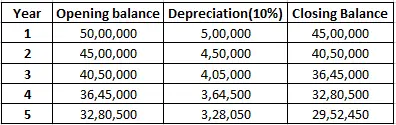

Now if the company decided to use the diminishing value method (or written down value method), then Rs 3,000 (30,000 x 10%) would be depreciated in the first year, and in the second year, the book value of the furniture would be Rs 27,000 (30,000-3,000). Hence depreciation for the second year would be Rs 2,700 (27,000 x 10%) and so on.

See less

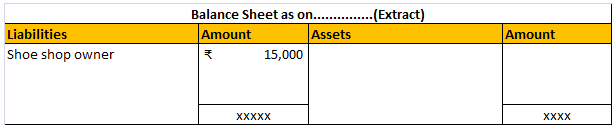

The provision for doubtful debts is the estimated amount of bad debts which will be uncollectible in the future. It is usually calculated as a percentage of debtors. The provision for a doubtful debt account has a credit balance and is shown in the balance sheet as a deduction from debtors. It is aRead more

The provision for doubtful debts is the estimated amount of bad debts which will be uncollectible in the future. It is usually calculated as a percentage of debtors. The provision for a doubtful debt account has a credit balance and is shown in the balance sheet as a deduction from debtors. It is a contra asset account which means an account with a credit balance.

When a business first sets up a provision for doubtful debts, the full amount of the provision should be debited to bad debts expense as follows.

In subsequent years, when provision is increased the account is credited, and when provision is decreased the account is debited. This is so because provision for doubtful debts is a contra account to debtors and has a credit balance, and is treated as a liability.

Effects of Provision for Doubtful Debts in financial statements:

For example, ABC Ltd had debtors amounting to Rs 50,000. It creates a provision of 5% on debtors.

Provision for Doubtful Debts = 50,000*5%

= 2,500

Journal entry for provision will be:

Effect on financial statements will be:

See less