Return inwards in simple terms means sending back goods by the customer to the seller. Simply speaking when your customer purchases items from your business but is not satisfied with the items so received they return those items back to you. Some of the reasons for sending back the items are statedRead more

Return inwards in simple terms means sending back goods by the customer to the seller. Simply speaking when your customer purchases items from your business but is not satisfied with the items so received they return those items back to you. Some of the reasons for sending back the items are stated below:

- Incorrect items delivered by the seller

- The excess amount delivered to the buyer

- Return of expired/ spoiled good

In such a case, the return is initiated by the buyer and a credit note is issued to the buyer, and the same is recorded in the books of accounts. Also, this return inward is deducted from the total sales.

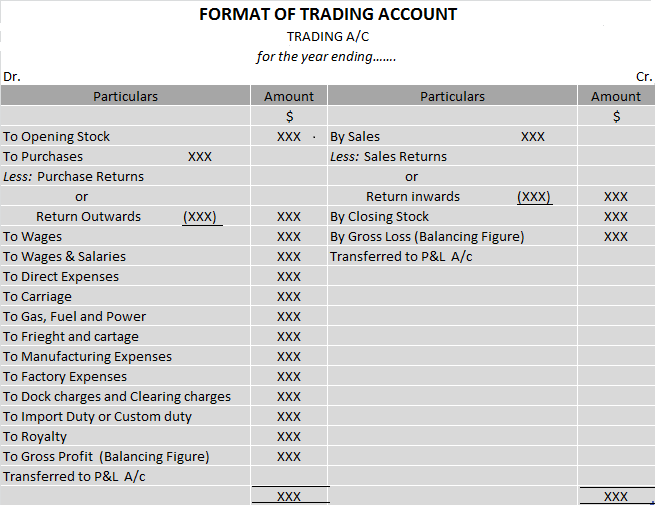

Example: M/s Pest ltd sold 4 units of fertilizers spraying tools of Rs 10,000 each to Mr. Zen. On inspection, he found 1 unit worth Rs 10,000 so received to be defective. Therefore the return of Rs 10,000 was initiated and goods were returned to the seller. A credit note of Rs 10,000 will be raised by the seller (M/s Pest ltd) to the buyer (Mr. Zen). The following adjustment will be shown in the trading account.

Return outwards means returning the goods by the buyer to the supplier. In layman language, when you purchase items for your business and you are not happy with the items then you may decide to return them.

In this case, a debit note is issued to the seller and is recorded in the books of accounts, and the same is reduced from the total purchases in the trading account so prepared.

Example: Suppose you are dealing in a business of clothing. You purchased 20 shirts for Rs.10,000 from a wholesale market. When you sold these shirts, you found 10 shirts worth Rs 5,000 to be defective which were returned by your customer. Therefore you will return these shirts to the wholesale market from where you purchased them. The following adjustment will be shown in the trading account.

See less

Yes, I agree with your statement that accounting information should be comparable. Comparability is one of the qualitative characteristics of accounting information. It means that users should be able to compare a company's financial statements across time and across other companies. Comparability oRead more

Yes, I agree with your statement that accounting information should be comparable.

Comparability is one of the qualitative characteristics of accounting information. It means that users should be able to compare a company’s financial statements across time and across other companies.

Comparability of financial statements is crucial due to the following reasons:

1. Intra-Firm Comparison:

Comparison of financial statements of two or more periods of the same firm is known as an intra-firm comparison.

Comparability of accounting information enables the users to analyze the financial statements of a business over a period of time. It helps them to monitor whether the firm’s financial performance has improved over time.

The intra-firm analysis is also known as Time Series Analysis or Trend Analysis.

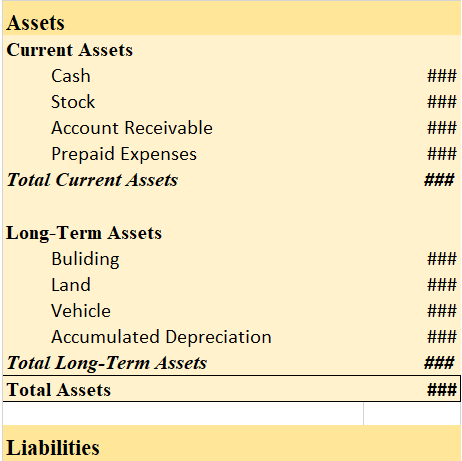

To understand intra-firm analysis, I have provided an extract of the balance sheet of ABC Ltd. for two accounting periods.

2. Inter-Firm Comparison:

Comparison of financial statements of two or more firms is known as an inter-firm comparison.

Inter-firm comparison helps in analyzing the financial performance of two or more competing firms in an industry. It enables the firm to know its position in the market in comparison to its competitors.

Inter-firm comparison is also known as Cross-sectional Analysis.

I’ve provided the balance sheets of Co. A and Co.B to make an inter-firm comparison.

Here is a piece of bonus information for you,

Sector Analysis – it refers to the assessment of economical and financial conditions of a given sector of a company/industry/economy. It involves the analysis of the size, demographic, pricing, competitive, and other economic dimensions of a sector of the company/industry/economy.

One more important thing to note here is that comparability can only be achieved when the firms are consistent in the accounting principles and standards they adopt. The accounting policies and standards must be consistent across different periods of the same firm and across different firms in an industry.

See less