A cheque that has been issued but yet not presented to the bank for payment is known as an unpresented cheque Generally what happens is when a cheque is issued to a party or say, creditor, the business immediately records them in the bank column of the cash book but the creditor might not present thRead more

A cheque that has been issued but yet not presented to the bank for payment is known as an unpresented cheque

Generally what happens is when a cheque is issued to a party or say, creditor, the business immediately records them in the bank column of the cash book but the creditor might not present them immediately to the bank for payment on the same date. The bank will only debit the account when it will be presented to it, therefore as long as the cheque remains unpresented there will be a difference in both the books i.e cash book and passbook.

Let me give you a short example of the above treatment

Suppose on 27th January, in the books of Mr. Shyam, the balance of the bank column as per the cash book is Rs 10,000. He received a cheque of Rs 5,000 from Mr. Hari, one of his debtors, which was sent to the bank for collection. The amount of the cheque was not collected by the bank until 31st January. Due to this, there arises a difference of Rs 5,000 in the cash book and pass book of Mr. Shyam.

Following will be the entry in Mr. Shyam cash book and passbook

In the books of Mr. Shaym

Cash book (bank column only)

| Date | Particulars | Bank (Rs) | Date | Particulars | Bank (Rs) |

| 27th Jan | To balance b/d | 10,000 | |||

| 27th Jan | To Hari | 5,000 | |||

| 31st Jan | By balance c/d | 15,000 | |||

| 15000 | 15000 |

Mr. Shyam

Bank Statement

| Date | Particulars | Debit (Withdraw) | Credit (Deposite) | Debit or Credit | Balance |

| 31st Jan | To balance b/d | credit | 10,000 |

How it is treated in the bank reconciliation statement?

There lies a temporary difference in both the books as the represented cheques will eventually be presented. Therefore we will not alter the cash book. The bank statement shows the greater amount of Rs 5,000 as compared to the cashbook, therefore we will debit the amount of unpresented cheque which will eventually make it balance to the level of bank statement.

See less

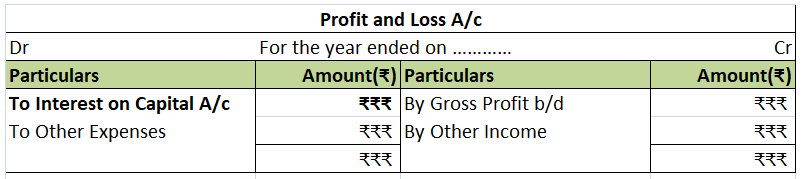

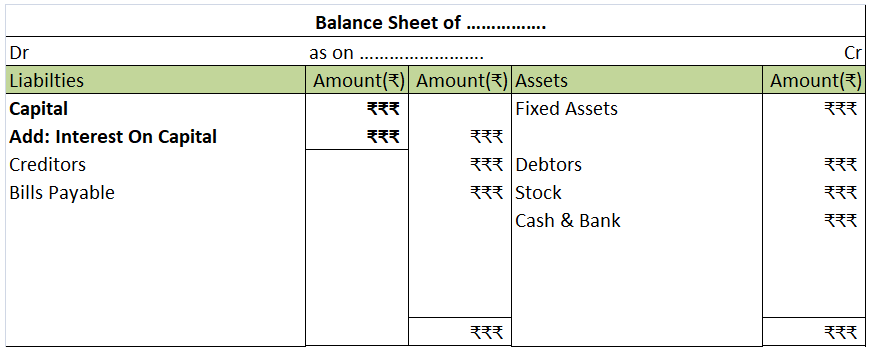

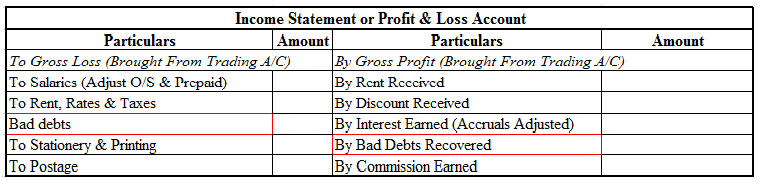

The "Income and Expenditure" account lists all the income and expenses incurred by the entity throughout the year. This account is very identical to the profit and loss account and is generally prepared on an accrual basis irrespective of whether the amount is received or paid. Non-profit organizatiRead more

The “Income and Expenditure” account lists all the income and expenses incurred by the entity throughout the year. This account is very identical to the profit and loss account and is generally prepared on an accrual basis irrespective of whether the amount is received or paid. Non-profit organizations (NPO) prepare this type of account to ascertain surplus earned or deficit incurred by them during the period.

Talking about the format of income and expenditure accounts we generally see that all the expenses are recorded on the debit side while all incomes are recorded on the credit side. One important thing to note is that items so recorded are revenue items while capital nature items are generally ignored because only current period items are recorded in this statement.

Since it is a Nominal account, we follow the golden rules to prepare this, stating “debit all expenses and losses and credit all incomes and gains”. The closing balance at the end shows the surplus or deficit for the year. If the balancing figure appears on the debit side it is surplus and if the balancing figure appears on the credit side it is a deficit for the entity.

Following is the format of income and expenditure account

See less