book value replacement value depreciable value market value

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization's activities. For example - Tax Authorities, Banks, Customers, Trade Unions, Government, Investors,Read more

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization’s activities.

For example – Tax Authorities, Banks, Customers, Trade Unions, Government, Investors, or Creditors.

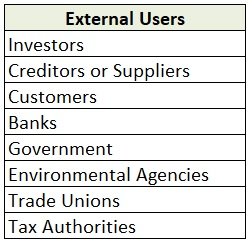

External Users:

- Investors – Investors are interested in the past performance and future earnings of the business. They want to track the performance of their business whether it is giving them any benefit or not. A business’s past information helps investors in assessing their investments.

- Creditors or Suppliers – Some suppliers provide goods and services on credit, and before providing any credit they check the company’s ability to pay. Creditors are interested in the company’s liquidity i.e to see if a company can fulfill short-term obligations.

- Customers – Customers are more interested in a company’s financial statement as they rely on them for goods and services. They check the ability of the company whether it is providing them good quality goods and will continue to provide them in future.

- Banks – Banks are most likely interested in the liquidity and profitability of the company. They keep track of whether the company can pay the debt when it is due along with interest.

- Government – The company’s activities are central to the economy and must be met by them. The government controls a company’s actions if they break a law or damage the environment.

- Environmental agencies – They keep an eye on organizations whether their activities are harming the environment or not.

- Trade unions – They take an active part in the decision-making process. They want to see the financial statements of the company and want to decide the compensation of the employees they represent.

- Tax authorities – They determine whether the business has declared the correct amount of tax in its tax returns. They conduct audits of the tax returns to verify them with the accounting records disclosed.

Here is a summary of external users

The total depreciation of an asset cannot exceed its 3. depreciable value. Depreciable value means the original cost of the asset minus its residual/salvage value. The asset's original cost is inclusive of the purchase price and other expenses incurred to make the asset operational. To put it simplRead more

The total depreciation of an asset cannot exceed its 3. depreciable value.

Depreciable value means the original cost of the asset minus its residual/salvage value. The asset’s original cost is inclusive of the purchase price and other expenses incurred to make the asset operational. To put it simply,

The accumulated depreciation on an asset can never exceed its depreciable value because depreciation is a gradual fall in the value of an asset over its useful life. Only a certain percentage of the asset’s book value/original cost is shown as depreciation every year. So, it is impossible/illogical for the accumulated depreciation of an asset to exceed its depreciable value.

Let me show you an example to make it more understandable,

Amazon installs machines to automate the job of packing orders. The original cost of the machine is $1,000,000. Now let’s assume,

The estimated useful life of the machine – 10 years.

Residual value at the end of 10 years – $50,000.

Method of depreciation – Straight-line method.

The depreciable value of the machine will be $950,000 (1,000,000 – 50,000). The depreciation for each year under SLM will be calculated as follows:

Depreciation = (Original cost of the asset – Residual/Salvage Value) / (Useful life of the asset)

Applying this formula, $95,000 (1,000,000 – 50,000/10) will be charged as depreciation every year. The accumulated depreciation at the end of 10 years will be $950,000 (95,000*10). As you can see, the accumulated depreciation ($950,000) of the machine does not exceed its depreciable value ($950,000).

Thus, the total depreciation of an asset cannot be more than its depreciable value.

See less