Meaning of Partnership Deed A Partnership Deed is a written agreement between partners who are willing to form a Partnership Firm. It is also called as a Partnership Agreement. Contents of a Partnership Deed A Partnership Deed shall mainly include the following contents: Name of the Partnership firmRead more

Meaning of Partnership Deed

A Partnership Deed is a written agreement between partners who are willing to form a Partnership Firm. It is also called as a Partnership Agreement.

Contents of a Partnership Deed

A Partnership Deed shall mainly include the following contents:

- Name of the Partnership firm

- Address of the Partnership firm

- Details of all the Partners

- Date of commencement of the Business

- The amount of capital contributed by each of the partners forming the Partnership firm

- The Profit sharing ratio (The Business profit shared among the partners on a ratio basis)

- The rate or amount of Interest on Capital & the rate or amount of Interest on drawings to each partner respectively.

- The salary payable to each of the partners of the firm.

- The rights, duties, and power of each partner of the firm.

- The duration of the existence of the firm

Importance of Partnership Deed

- Proper regulation of duties, liabilities, and rights of the partners are made in the partnership deed and hence there cannot be any issue during the course of the business.

- There can be no disputes between the partners upon Profit sharing, salary, commission, interest on capital, and interest on drawings.

- A partnership Deed acts as Legal proof for the conduct of the business and is used for many other registrations such as GST registration, and other related purposes.

Format of a Partnership Deed

The Partnership Deed shall originally be executed on an Indian Non-Judicial stamp paper.

The format of the Partnership deed is given below with an assumption that 4 partners are forming the Partnership.

PARTNERSHIP DEED

This deed of partnership is made on [Date, Month, Year] between:

1. [First Partner’s Name], [Son/Daughter] of [Mr. Father’s Name], residing at [Address Line 1, Address Line 2, City, State, Pin Code] hereinafter referred to as FIRST PARTNER.

2. [Second Partner’s Name], [Son/Daughter] of [Mr. Father’s Name], residing at [Address Line 1, Address Line 2, City, State, Pin Code] hereinafter referred to as SECOND PARTNER.

3. [Third Partner’s Name], [Son/Daughter] of [Mr. Father’s Name], residing at [Address Line 1, Address Line 2, City, State, Pin Code] hereinafter referred to as THIRD PARTNER.

4. [Fourth Partner’s Name], [Son/Daughter] of [Mr. Father’s Name], residing at [Address Line 1, Address Line 2, City, State, Pin Code] hereinafter referred to as FOURTH PARTNER.

Whereas, the parties hereto have agreed to commence business in partnership and it is expedient to have a written instrument of partnership. Now, this partnership deed witnesses as follows:

1. BUSINESS ACTIVITY

The parties hereto have mutually agreed to carry on the business of [Description of Business Activity Proposed].

2. PLACE OF BUSINESS

The principal place of the partnership business will be situated at [Address Line 1, Address Line 2, City, State, Pin Code]

3. DURATION OF PARTNERSHIP

The duration of the partnership will be at will.

4. CAPITAL OF THE FIRM

Initially, the capital of the firm shall be Rs. [Total Partners Contribution].

5. PROFIT SHARING RATIO

The profit or loss of the firm shall be shared equally among all the partners and transferred to the partner’s current account.

6. MANAGEMENT

The [First Partner] of the firm shall be Managing Partner and he will look after all the day-to-day transactions of the firm and any legal activities in the name of the firm and the remaining partners shall cooperate to do so.

7. OPERATION OF BANK ACCOUNTS

The firm shall open a current account in the name of [Partnership Firm Name] at any bank and such account shall be operated by [First Partner] and [Second Partner] jointly as declared from time to time to the Banks.

8. BORROWING

The written consent of all Partners will be required for the partnership to avail credit facilities from any financial institution.

9. ACCOUNTS

The firms shall regularly maintain in the ordinary course of business, true and correct accounts of all its transactions and also of all its assets and liabilities, the property books of account, which shall ordinarily be kept at the firm’s place of business. The accounting year shall be the financial year from 1st April onwards and the balance sheet shall be properly audited and the same shall be signed by all the Partners. Every Partner shall have access to the books and the right to verify their correctness.

10. RETIREMENT

If any partner shall at any time during the subsistence of the partnership, be desirous of retiring from the firm, it shall be competent from his to do so, provided he shall give at least one calendar month’s notice of his intention of doing so. The remaining partner shall pay the retiring partner or his legal representatives of the deceased partner, the purchase money of his share in the assets of the firm.

11. DEATH OF PARTNER

In the event of the death of any partners, one of the legal representatives of the deceased partner shall become the partner of the firm and in the event, the legal representative shows their denial to point the firm, they shall be paid part of the purchase amount calculated as on the date of the death of the partner.

12. ARBITRATION

Whenever there by any difference of opinion or any dispute between the partners shall refer the same to the arbitration of one person. The decision of the arbitration so nominated shall be final and binding on all partners, such arbitration proceedings shall be governed by Indian Arbitration Act, which is in force.

In witness whereof, this deed of partnership is signed sealed, and delivered this [Day, Month, Year] at [City, State]:

FIRST PARTNER SECOND PARTNER

[Address Line 1] [Address Line 1]

[Address Line 2] [Address Line 2]

[City, State, Pin Code] [City, State, Pin Code]

THIRD PARTNER FOURTH PARTNER

[Address Line 1] [Address Line 1]

[Address Line 2] [Address Line 2]

[City, State, Pin Code] [City, State, Pin Code]

WITNESS ONE WITNESS TWO

[Address Line 1] [Address Line 1]

[Address Line 2] [Address Line 2]

[City, State, Pin Code] [City, State, Pin Code]

There are three types of businesses that can be commenced, they are sole proprietorship, partnership, and joint-stock company. As we all know, to start any business a certain sum of money has to be invested by the owner which is known as the capital of the business in terms of accounting. In companiRead more

There are three types of businesses that can be commenced, they are sole proprietorship, partnership, and joint-stock company. As we all know, to start any business a certain sum of money has to be invested by the owner which is known as the capital of the business in terms of accounting.

In companies, commencement is a declaration issued by the company’s directors with the registrar stating that the subscribers of the company have paid the amount agreed. In a sole proprietorship, the business can be commenced with the introduction of any asset such as cash, stock, furniture, etc.

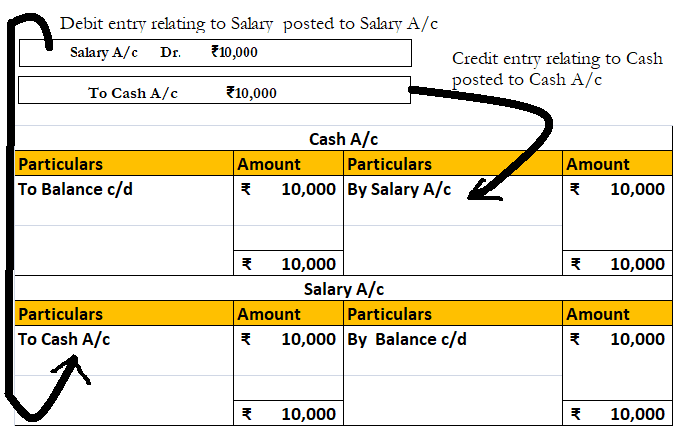

Journal entry

In the journal entry, “Started business with Cash”

As per the golden rules of accounting, the cash a/c is debited because we bring in cash to the business, and as the rule says “debit what comes in, credit what goes out.” Whereas the capital a/c is credited because “debit all expenses and losses, credit all incomes and gains”

As per modern rules of accounting, cash a/c is debited as cash is a current asset, and assets are debited when they increase. Whereas, on the increment on liabilities, they are credited, therefore, capital a/c is credited.

Therefore, the entry we’ll be passing is-

See less