Here I've prepared the Income & Expenditure A/c. Income & Expenditure A/c for the year ended 31st March 2021 Expenditure Amt Income Amt To Salary 4,80,000 By Subscriptions 9,00,000 To Rent 50,000 By Donations 10,000 To Stationery 20,000 To Loss on sale ofRead more

Here I’ve prepared the Income & Expenditure A/c.

Income & Expenditure A/c for the year ended 31st March 2021

| Expenditure | Amt | Income | Amt |

| To Salary | 4,80,000 | By Subscriptions | 9,00,000 |

| To Rent | 50,000 | By Donations | 10,000 |

| To Stationery | 20,000 | ||

| To Loss on sale of furniture (WN) | 10,000 | ||

| To Surplus | 3,50,000 | ||

| 9,10,000 | 9,10,000 |

Working Note: Calculation of Loss on sale of furniture

The following calculation is made to identify the loss incurred on the sale of furniture.

| Particulars | Amt |

| Book Value of Furniture | 40,000 |

| Less: Sale Value of Furniture | 30,000 |

| Loss on Sale of Furniture | 10,000 |

See less

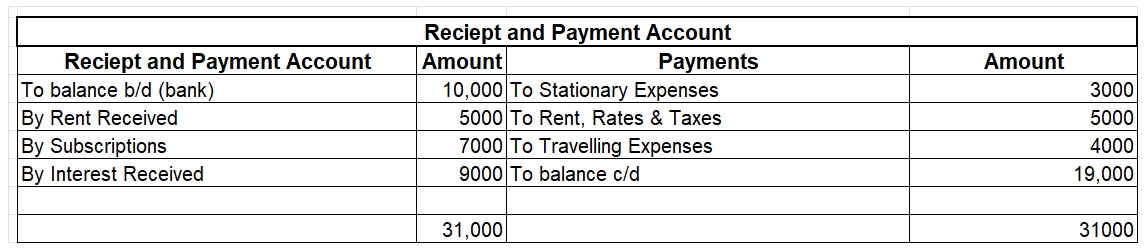

Receipts and payment account is a summary of cash transactions prepared at the end of the accounting period from the cash book where the transactions are recorded in chronological order. It is an Asset/ Real Account that records both revenue and capital receipts and payments. It is mainly prepared fRead more

Receipts and payment account is a summary of cash transactions prepared at the end of the accounting period from the cash book where the transactions are recorded in chronological order. It is an Asset/ Real Account that records both revenue and capital receipts and payments. It is mainly prepared for non-profit organizations and helps in the preparation of final accounts.

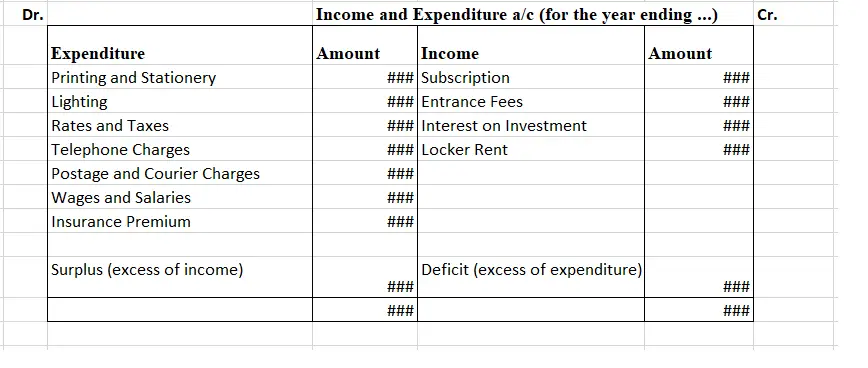

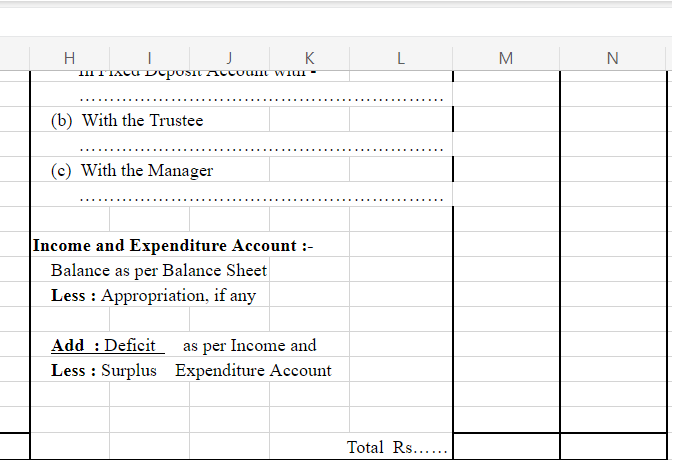

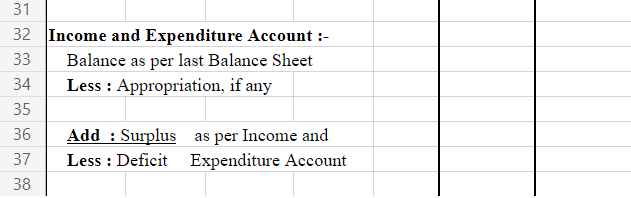

Proforma

Income and Expenditure Account is an account prepared by not-for-profit organizations to see whether the income of a particular period is sufficient to cover the expenses of that period. If the revenue is more than the expenses, it is known as “Surplus” or “Excess of Income over Expenditure” and if the expenses are more than Income, it is known as “Deficit” or “Excess of Expenditure over Income”. The account is prepared on the accrual basis of accounting i.e. all revenue incomes whether received or not and all revenue expenditures of the period whether paid or not are taken into account. However, in case of surplus, the money is not distributed among the members. Similarly, if there is a deficit it is not borne by the members.

Proforma

See less