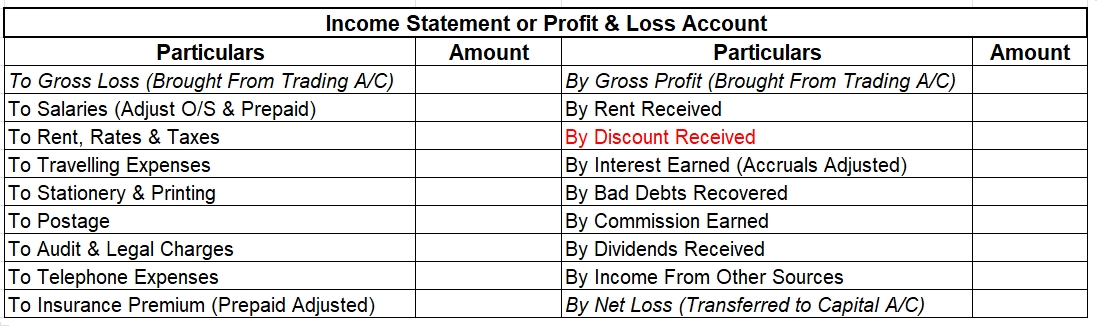

The profit earned by an entity is determined through the profit and loss account. All the expenses are recorded on the debit side of the profit and loss account while all the incomes are recorded on the credit side. The profit is shown as the credit balance of profit and loss A/c. When the sum of itRead more

The profit earned by an entity is determined through the profit and loss account. All the expenses are recorded on the debit side of the profit and loss account while all the incomes are recorded on the credit side.

The profit is shown as the credit balance of profit and loss A/c. When the sum of items on the debit side of a profit and loss account is less than the sum of those on the credit side, it implies profit while when the sum of the items on the credit side is less than the sum of those on the debit side, it implies a loss for the entity.

The Reason for Credit

Profit is recorded as an increase in equity

To understand the reason why profit is recorded as a credit balance, we must first understand the basic principle of debit and credit.

The basic principle of debits and credits is that debits increase asset accounts and decrease liability and equity accounts while credits decrease asset accounts and increase liability and equity accounts.

The revenue that a company earns is credited to the income account and increases equity.

The expenses that a company incurs to earn that revenue are debited to the expense account and decrease equity.

The difference between revenue and expenses is the profit, which is recorded as an increase in equity.

Increase in equity due to revenue – decrease in equity due to expense = profit

Gross Profit Vs Net Profit

Revenue is the total income that a business or profession earns. Profit is the excess revenue that remains after reducing all expenses from it.

Gross profit is the profit that a company earns after reducing the cost of goods sold from sales revenue while net profit is the profit that a business earns after reducing the total of all its direct and indirect expenses from its direct as well as indirect allowable business income.

Conclusion

The basic principle of debit and credit governs the classification of profit as a debit or credit. Since profit increases our equity, it is a credit.

In the case of a company, it belongs to the shareholders. It is usually recorded in the retained earnings account. Profit can be reinvested in the business or can be distributed as a dividend. In the case of a sole proprietorship, the profit belongs to the owner and is recorded in the owner’s capital account.

See less

Non-debt capital receipts As we're aware, there are two main sources of the government’s income — revenue receipts and capital receipts. Revenue receipts are all those receipts that neither create any liability nor cause any reduction in assets for the government, whereas, capital receipts are thoseRead more

Non-debt capital receipts

As we’re aware, there are two main sources of the government’s income — revenue receipts and capital receipts. Revenue receipts are all those receipts that neither create any liability nor cause any reduction in assets for the government, whereas, capital receipts are those money receipts of the government that either create a liability for a government or cause a reduction in assets.

Revenue receipts comprise both tax and non-tax revenues while capital receipts consist of capital receipts and non-debt capital receipts. Non-debt capital receipt is a part of capital receipt.

Definition

Non-debt capital receipts, also known as NDCR, are the taxes and duties levied by the government forming the biggest source of its income. Those receipts of the government lead to a decrease in assets, and not an increase in liabilities. It accounts for just 3% of the central government’s total receipts.

The union government usually lists non-debt capital receipts in two categories:

For Example – Disinvestment and recovery of loans are non-debt creating capital receipts.

See less