Yes, non-current assets are also known as fixed assets. These are long-term assets that are not intended for sale but are used by a company in its business operations. Examples of non-current assets include property, plant, and equipment, as well as intangible assets like patents and trademarks. TheRead more

Yes, non-current assets are also known as fixed assets. These are long-term assets that are not intended for sale but are used by a company in its business operations.

Examples of non-current assets include property, plant, and equipment, as well as intangible assets like patents and trademarks. These assets are recorded on a company’s balance sheet and are reported at their historical cost or at their fair market value, depending on the type of asset.

See less

Profits earned by a firm are not completely distributed to its owners, some of the profits are retained for various purposes. Reserves are profits that are apportioned or set aside to use in the future for a specific or general purpose. Reserves follow the Conservative Principle of accounting. ReveRead more

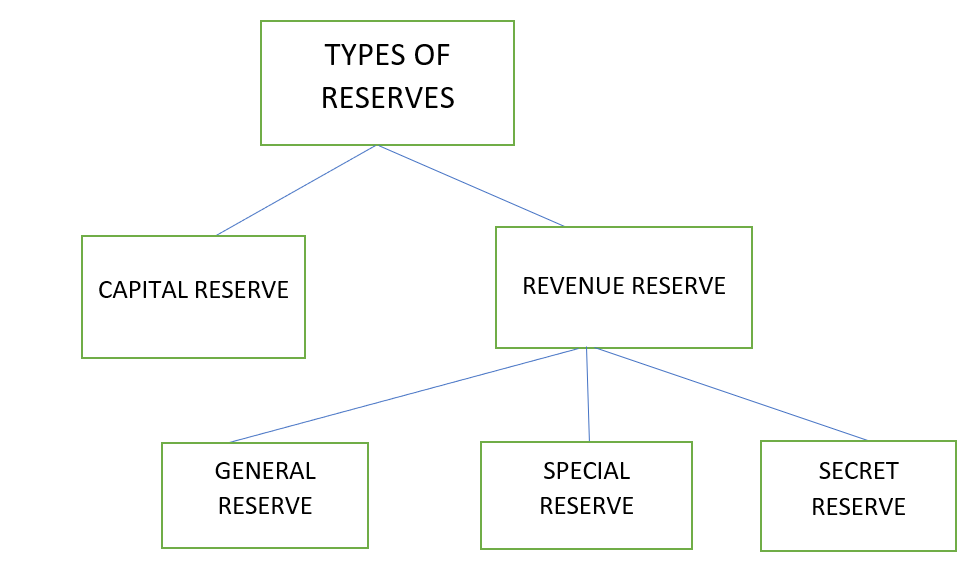

Profits earned by a firm are not completely distributed to its owners, some of the profits are retained for various purposes. Reserves are profits that are apportioned or set aside to use in the future for a specific or general purpose. Reserves follow the Conservative Principle of accounting.

Revenue reserve is created from the net profits of a company during a financial year. Revenue reserve is created from revenue profit that a company earns from the daily operations of the business.

Various types of reserves are:

Different parts of profit are apportioned to create a different reserve and those reserves can only be used for purposes as defined.

While accounting for Revenue Reserve, the profit decided to transfer to Revenue Reserve are first transferred to Profit and Loss Appropriation Account and then to Revenue Reserve Account. In the balance sheet, Revenue Account is shown under the Capital and Reserves head.

Uses of Revenue Reserve:

Example:

Given that Revenue Reserve Account stands at Rs 1,00,000 and the company wants to distribute Rs. 40,000 as dividend to its shareholders. The treatment of this transaction in the financial statements will be-

Particulars Amount (Rs.)

Revenue Reserve Account 1,00,000

(less) Dividend distributed (40,000)

The amount shown in Balance Sheet 60,000

See less