Ledger posting The process of entering all transactions from journal to ledger is called ledger posting. Each ledger account contains an individual asset, person, revenue, or expense. As we're aware the journal records all the transactions of the business. Posting to the ledger account not only helpRead more

Ledger posting

The process of entering all transactions from journal to ledger is called ledger posting. Each ledger account contains an individual asset, person, revenue, or expense. As we’re aware the journal records all the transactions of the business.

Posting to the ledger account not only helps the proper maintenance of the ledger book but also helps in reflecting a permanent summary of all the journal accounts. In the end, all the accounts that are entered and operated in the ledger are closed, totaled, and balanced.

Balancing the ledger means finding the difference between the debit and credit amounts of a particular account, it’s done on the day of closing of the accounting year. Sometimes journal entries are made and maintained monthly. Therefore, the balancing of the ledger’s date depends on the business’ closing date and the way a business maintains its books of accounts.

Example

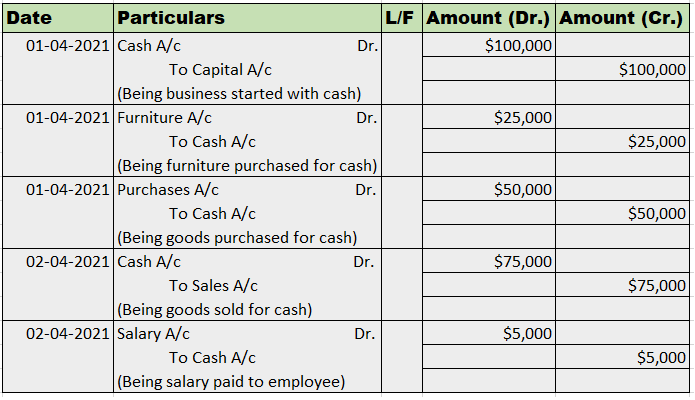

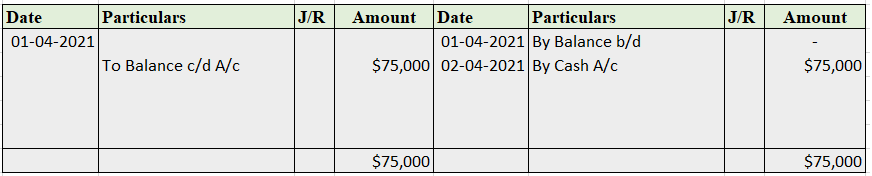

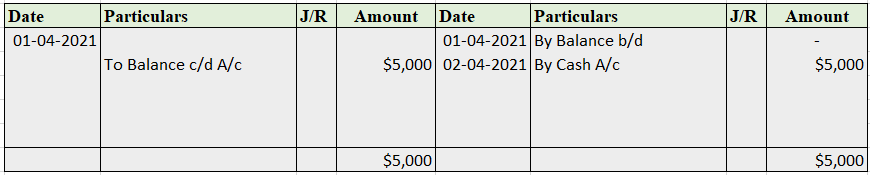

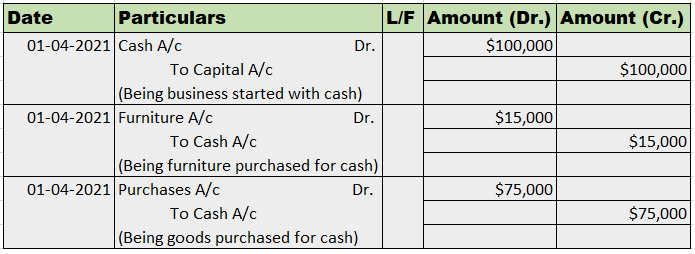

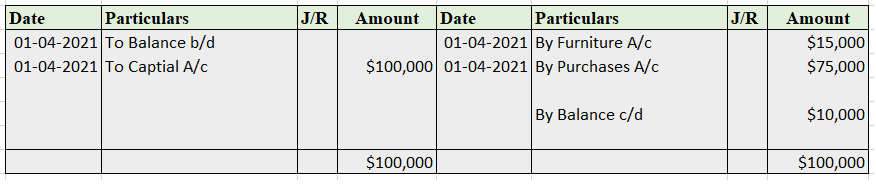

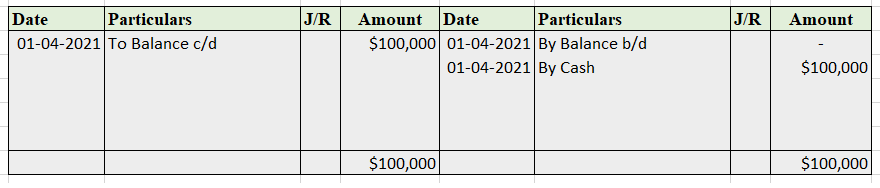

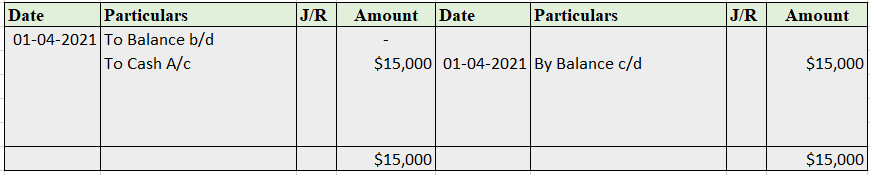

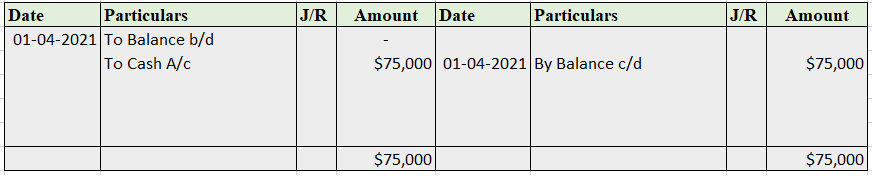

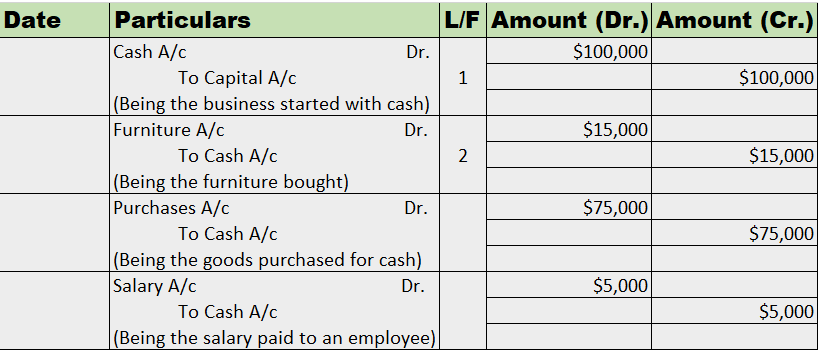

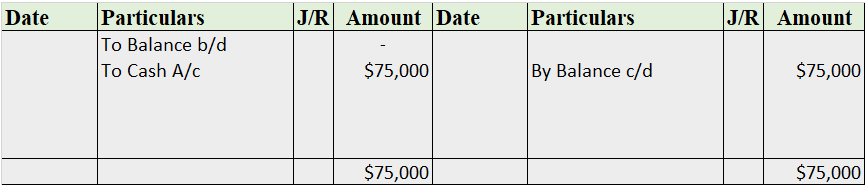

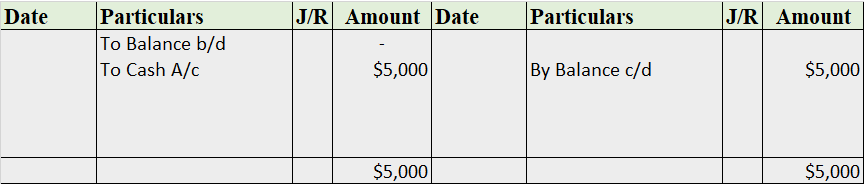

Mr. Jack Sparrow decided to start a new clothing business. On 1st April 2021, He started the business with a total sum of $100,000 cash. He purchased furniture, including desks and shelves for $25,000. Mr. Sparrow then decided to start with women’s clothing and purchased a complete range of clothes from the wholesale market for $50,000. On the next day, he sold all the stock for $75,000. He also hired a worker for $5,000.

We need to journalize these transactions and post them into the ledger account.

Journal Entries

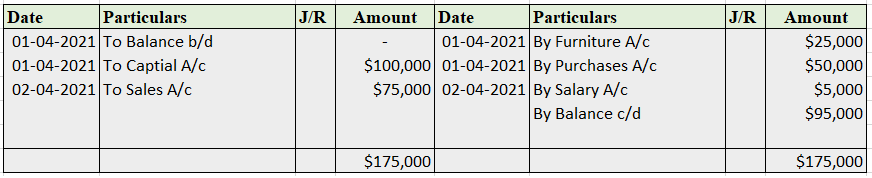

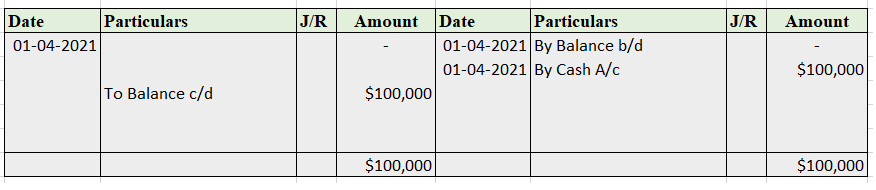

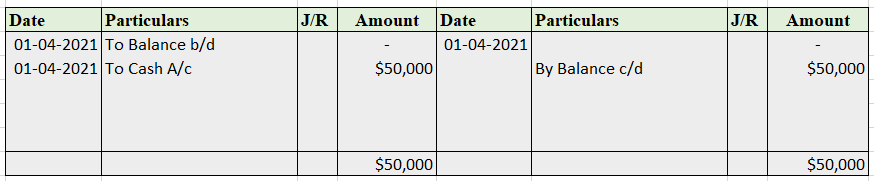

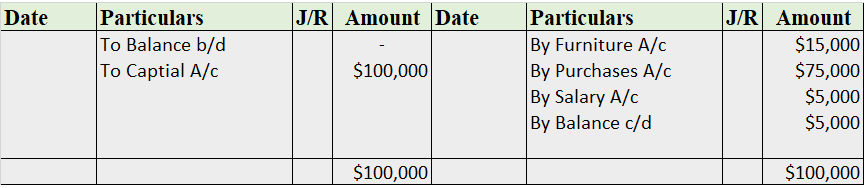

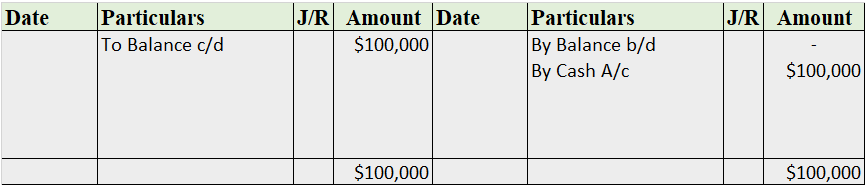

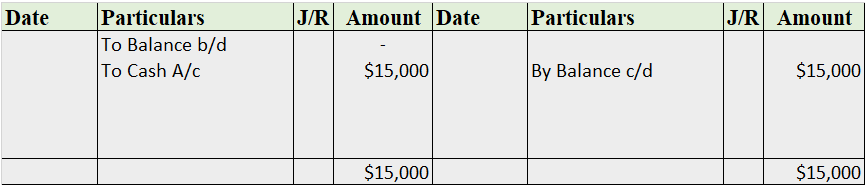

Ledger Accounts

Cash A/c

Capital A/c

Purchases A/c

Sales A/c

Salary A/c

Sales Return is shown on the debit side of the Trial Balance. Sales Return is also called Return Inward. Sales Return refers to those goods which are returned by the customer to the seller of the goods. The goods can be returned due to various reasons. For example, due to defects, quality differenceRead more

Sales Return is shown on the debit side of the Trial Balance.

Sales Return is also called Return Inward.

Sales Return refers to those goods which are returned by the customer to the seller of the goods. The goods can be returned due to various reasons. For example, due to defects, quality differences, damaged products, and so on.

In a business, sales is a form of income as it generates revenue. So, when the customer sends back those goods sold earlier, it reduces the income generated from sales and hence goes on the debit side of the trial balance as per the modern rule of accounting Debit the increases and Credit the decreases.

For Example, Mr. Sam sold goods to Mr. John for Rs 500. Mr. John found the goods damaged and returned those goods to Mr. Sam.

So, here Sam is the seller and John is the customer.

The journal entry for sales return in the books of Mr. Sam will be

Treatment in Trial Balance

See less