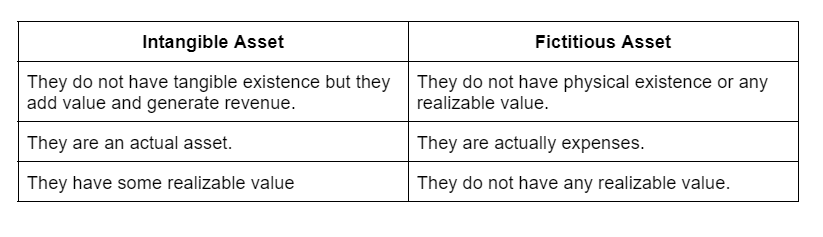

The answer is B. False. Before jumping on the solution to know why goodwill is not fictitious, we need to know what are fictitious assets? Fictitious assets are false assets or not true assets. These are not assets but expenses & losses that are not written off from the profit & loss accountRead more

The answer is B. False. Before jumping on the solution to know why goodwill is not fictitious, we need to know what are fictitious assets?

Fictitious assets are false assets or not true assets. These are not assets but expenses & losses that are not written off from the profit & loss account but shown in the balance sheet as assets under the head miscellaneous expenditure. For example preliminary expenses, loss on issue of debentures, etc.

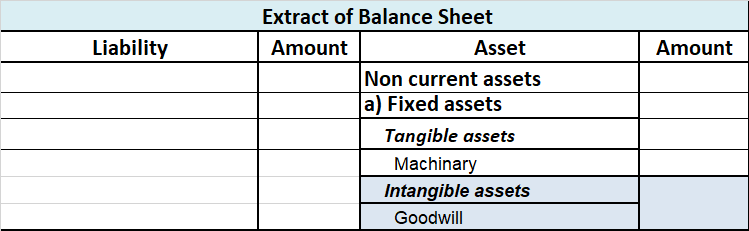

Goodwill is not a fictitious asset but an intangible asset which means it has no actual physical appearance and cannot be touched and felt like other assets like buildings and machinery. It is nothing but a firm’s reputation which can be sold just like other assets help the business grow and earn revenue. Goodwill is shown in the balance sheet as follows:

Definition Goodwill is an intangible asset that places an enterprise in an advantageous position due to which the enterprise is able to earn higher profits without extra effort. For example, if the enterprise has rendered good services to its customers, it will be satisfied with the quality of its sRead more

Definition

Goodwill is an intangible asset that places an enterprise in an advantageous position due to which the enterprise is able to earn higher profits without extra effort.

For example, if the enterprise has rendered good services to its customers, it will be satisfied with the quality of its services, which will bring them back to the enterprise.

Features

The value of goodwill is a subjective assessment of the valuer.

• It helps in earning higher profits.

• It is an intangible asset.

• It is an attractive force that brings in customers to the business.

• It has realizable value when the business is sold out.

Need for goodwill valuation

The need for the valuation of goodwill arises in the following circumstances :

• When there is a change in profit sharing ratio.

• When a new partner is admitted.

• When partner retires or dies.

• When a partnership firm is sold as a going concern.

• When two or more firms amalgamate.

Classification of goodwill

Goodwill is classified into two categories:

• Purchased goodwill

• Self-generated goodwill

Purchased goodwill :

Is that goodwill acquired by the firm for consideration whether paid or kind?

For example: when a business is purchased and purchase consideration is more than the value of net assets the difference amount is the value of purchase goodwill.

Self-generated goodwill

It is that goodwill that is not purchased for consideration but is earned by the management’s efforts.

It is an internally generated goodwill that arises from a number of factors ( such as favorable location, efficient management, good quality of products, etc ) that a running business possesses due to which it is able to earn higher profits.

Methods of valuation

1. Average profit method

2. Super profit method

3. Capitalization method

Average profit method: goodwill under the average profit method can be calculated either by :

• Simple average profit method or

• Weighted average profit method

See less