The installation expenses for a new machinery will be debited to the "Machinery A/c". Installation expenses are the expense incurred to bring an asset to a working condition where it can be used. For example, installation charges are incurred on machinery to make it operational. Installation chargesRead more

The installation expenses for a new machinery will be debited to the “Machinery A/c“. Installation expenses are the expense incurred to bring an asset to a working condition where it can be used. For example, installation charges are incurred on machinery to make it operational.

Installation charges will be capitalized along with the cost of machinery. It is so because this expense is concerning the machinery and any expense directly related to an asset should be capitalized, as an asset will be with the business for a longer period of time.

This charge will be incurred only once as a part of bringing the machinery to its working condition, and hence it should be capitalized and should be added to the cost of the machine. The whole amount will be shown in the balance sheet on the asset side as a Fixed Asset.

This charge will not be shown in Profit and Loss A/c as it reflects all the revenue expenditure incurred in the period.

Example:

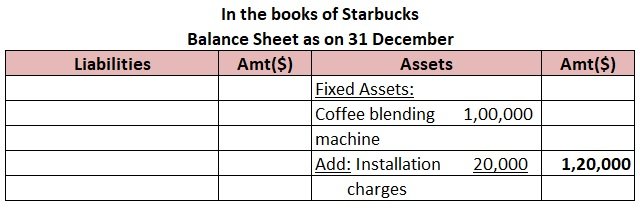

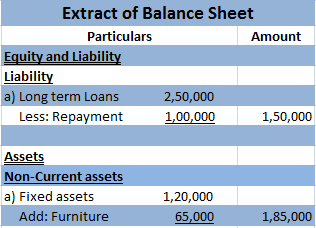

Starbucks purchased a coffee blending machine for the business purpose for $1,00,000. The installation expense incurred on it to make it operational was $20,000. How will Starbucks record this in the Balance Sheet on 31 December?

In the Balance Sheet, Starbucks will add the installation expense incurred on the machine to the cost of the machine as it is the cost incurred to make the machine operational for further business use. Hence, the cost of $20,000 will be shown along with the cost of the coffee blending machine ($1,00,000+$20,000=$1,20,000)

See less

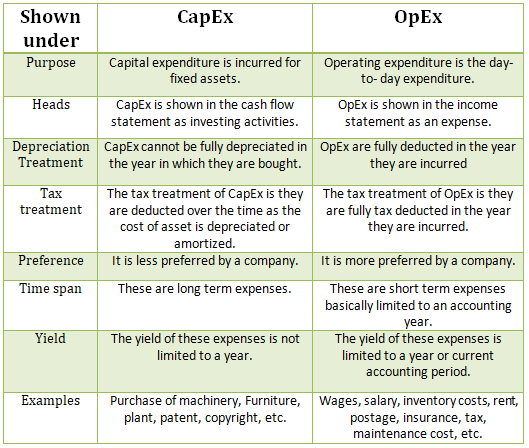

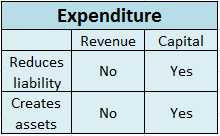

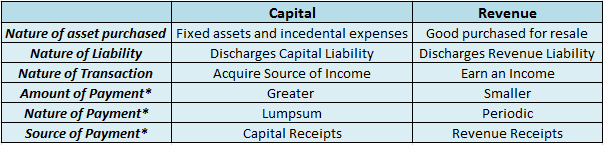

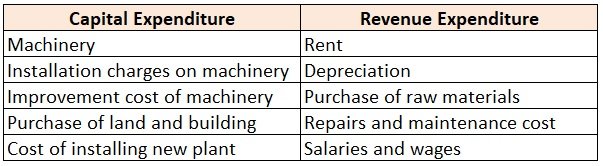

Capital Expenditure Capital expenditure refers to the money a business spends to buy, maintain, or improve the quality of its assets. Capital expenditures are the expenses incurred by an organization for long-term benefits, i.e on the long-term assets which help in improving the efficiency or capaciRead more

Capital Expenditure

Capital expenditure refers to the money a business spends to buy, maintain, or improve the quality of its assets. Capital expenditures are the expenses incurred by an organization for long-term benefits, i.e on the long-term assets which help in improving the efficiency or capacity of the company. These expenses are borne by the company to boost its earning capacity.

The investment done by the companies on assets is capital in nature and through capital expenditure, the company may use it for acquiring new assets or may use it in the maintenance of previous ones. These expenditures are added to the asset side of the balance sheet.

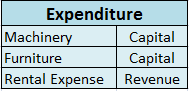

Example: Purchase of machinery, patents, copyrights, installation of equipment, etc.

Revenue Expenditure

Revenue expenditure refers to the routine expenditures incurred by the business to manage day-to-day expenses. They are incurred for a shorter duration and are mostly limited to an accounting year. These expenses are borne by a company to sustain its profitability. These expenditures are shown in the income statement.

These expenditures do not increase the revenue but stay maintained. These expenses are not capitalized.

They are divided into two sub-categories:

Example: Wages, salary, insurance, rent, electricity, taxes, etc.

See less