Interest on drawings Drawings refer to the money withdrawn by owners/partners for personal use from the business. The drawings, in accounting terms, can be of any type. It can be cash withdrawn from business or furniture or car etc. Drawings are money or assets that are withdrawn from a company by iRead more

Interest on drawings

Drawings refer to the money withdrawn by owners/partners for personal use from the business. The drawings, in accounting terms, can be of any type. It can be cash withdrawn from business or furniture or car etc. Drawings are money or assets that are withdrawn from a company by its owners for personal use and must be recorded as a reduction of assets. It’s paid back to the business with some interest.

Interest on drawings is an income for the business and reduces the capital of the owner. Interest on drawings is the amount of interest paid by the partners, calculated concerning the period for which the money was withdrawn.

- It’s an income for the business. Hence, credited to P&L Appropriation A/c.

- It’s an expense for the owner/partner. Therefore, debited to owner’s/partner’s capital a/c

- Interest on drawings is charged to the partners only when there is an agreement made among the partners in this regard or if it is mentioned in the Partnership Deed.

Formulae for Interest on drawings

There are three formulae used for calculating the interest on drawings. They are:

1. Simple Method: In this method, as the name suggests, the amount of interest on drawings is calculated simply for the time the amount has been utilized.

Interest on Drawings = Amount of drawings × Rate/100 × No. of Months/12

2. Product Method: This method is used when-

- Drawings are made of unequal amounts at irregular intervals of time. Then this formula is used-

Interest on Drawings = Total of Products × Rate/100 × 1/12

- When drawings are made of equal amounts at regular/equal intervals of time. Then interest on drawings can be calculated on the total of the amount drawn, for the average of the period applicable to the first and last installment.

Interest on Drawings= Total amount of drawings × Rate/ 100 × Average Period/12

Also, note-

Average Period = (No. of months left after first drawings+ No. of months left after last drawings)/2

Example:

Harish withdrew equal amounts at the beginning of every month for 9 months. Total drawings amounted to ₹6,000. Calculate the interest on drawings charged if the rate was 6% p.a.

Solution:

Average period = (No. of months left after first drawings+ No. of months left after last drawings)/2 = (9+1)/2 = 5 months

Interest on Drawings = Total of drawings × Rate/100 × 5/12

Journal entry for interest on drawings:

Interest transferred to Profit & Loss A/c:

See less

Introduction Working capital refers to the capital which is required by an enterprise to smoothly run its daily operations. It is the measure of the short-term liquidity of a business. Working capital is the total of the current assets of a business, net of its current liabilities. Working capitalRead more

Introduction

Working capital refers to the capital which is required by an enterprise to smoothly run its daily operations.

It is the measure of the short-term liquidity of a business.

Working capital is the total of the current assets of a business, net of its current liabilities.

Working capital = Current Assets – Current Liabilities

The working capital consists of cash, accounts receivable and inventory of raw materials and finished goods fewer accounts payable and other short-term liabilities.

Without a proper level of working capital, a business cannot maintain regular production and pay its creditors and expenses.

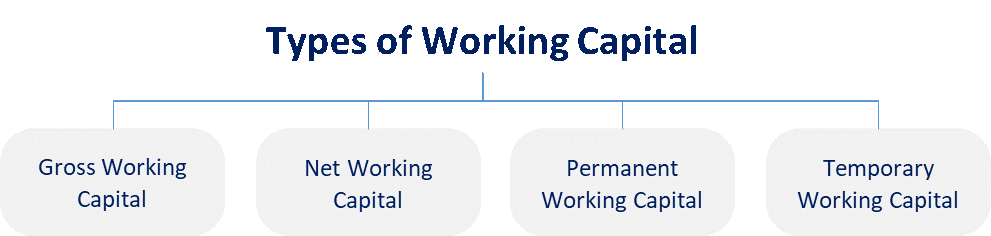

Hence, for proper management of working capital, it is divided into types:

I have discussed them below:

Permanent Working Capital

It is the fixed level or minimum level of working capital that an enterprise needs to maintain to ensure production at the normal capacity and pay for its daily expenses. It is independent of the level of production.

It is also known as fixed working capital.

By ‘permanent’, it does not mean that it will forever remain at the same level or amount but it may change if the overall production capacity changes. But such changes in permanent working capital are not often.

Temporary Working Capital

It is the level of working capital that depends upon the level of production of a business. It is the excess working capital over the permanent capital that is required to meet seasonal high demand.

It is also known as fluctuating working capital because it tends to change often depending on the level of production.

Temporary working capital is required when high production is required to meet seasonal demands.

For example, a bakery will need more working capital to meet the increased demand for cakes and pastry during Christmas season

Graph showing permanent and temporary working capital

Here, the temporary working capital is fluctuating whereas the permanent working capital is gradually increasing with time.

See less