One of the main purposes of accounting is to provide financial data to its users so that decisions are taken at an appropriate time. These users of accounting information are broadly classified into (a) internal users and (b) external users. Since the question concentrates on internal users I’ll beRead more

One of the main purposes of accounting is to provide financial data to its users so that decisions are taken at an appropriate time. These users of accounting information are broadly classified into (a) internal users and (b) external users. Since the question concentrates on internal users I’ll be explaining internal users of accounting information in detail.

Internal users are people within an organization/business who need accounting information to make day-to-day decisions.

The various internal users of accounting information include:

- Owners/Promoters/Directors:

Owners are the people who contribute capital to the business and therefore they are interested to know the profit earned or loss incurred by the business as well as the safety of their capital. In the case of a Sole Proprietorship, the proprietor is the owner of the business. In the case of a Partnership, the partners are considered as the owners of the firm.

The use for them: To know how the business is doing financially, owners need to know the profit and loss reflected in the financial statements.

- Management:

Management is responsible for setting objectives, formulating plans, taking informed decisions, and ensuring that pre-planned objectives are met within the stipulated time period.

The use for them: To achieve objectives, management needs accounting information to make decisions related to determining the selling price, budgeting, cost control and reduction, investing in new projects, trend analysis, forecasting, etc.

- Employees/Workers:

Employees and workers are the ones who implement the plans set by the management. Their well-being is dependent on the profitability of the business.

The use for them: They are interested to check the financial statements so that they can get a better knowledge of the business. Some organizations also give their employees a share in their profits in the form of a bonus at the year-end. This also creates an interest in the employees to check the financial statements.

See less

Generally, Assets are classified into two types. Non-Current Assets Current Assets Non-Current Asset Noncurrent assets are also known as Fixed assets. These assets are an organization's long-term investments that are not easily converted to cash or are not expected to become cash within an acRead more

Generally, Assets are classified into two types.

Non-Current Asset

Noncurrent assets are also known as Fixed assets. These assets are an organization’s long-term investments that are not easily converted to cash or are not expected to become cash within an accounting year.

In general terms, In accounting, fixed assets are assets that cannot be converted into cash immediately. They are primarily tangible assets used in production having a useful life of more than one accounting period. Unlike current assets or liquid assets, fixed assets are for the purpose of deriving long-term benefits.

Unlike other assets, fixed assets are written off differently as they provide long-term income. They are also called “long-lived assets” or “Property Plant & Equipment”.

Examples of Fixed Assets

Valuation of Fixed asset

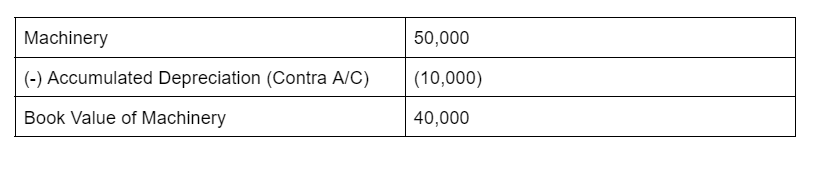

fixed assets are recorded at their net book value, which is the difference between the “historical cost of the asset” and “accumulated depreciation”.

“Net book value = Historical cost of the asset – Accumulated depreciation”

Example:

Hasley Co. purchases Furniture for their company at a price of 1,00,000. The Furniture has a constant depreciation of 10,000 per year. So, after 5 years, the net book value of the computer will be recorded as

1,00,000 – (5 x 10,000) = 50,000.

Therefore, the furniture value should be shown as 50,000 on the balance sheet.

Presentation in the Balance Sheet

Both current assets and non-current assets are shown on the asset side(Right side) of the balance sheet.

Difference between Current Asset and Non-Current Asset

Current assets are the resources held for a short period of time and are mainly used for trading purposes whereas Fixed assets are assets that last for a long time and are acquired for continuous use by an entity.

The purpose to spend on fixed assets is to generate income over the long term and the purpose of the current assets is to spend on fixed assets to generate income over the long term.

At the time of the sale of fixed assets, there is a capital gain or capital loss but at the time of the sale of current assets, there is an operating gain or operating loss.

The main difference between the fixed asset and current asset is, although both are shown in the balance sheet fixed assets are depreciated every year and it is valued by (the cost of the asset – depreciation) and current asset is valued as per their current market value or cost value, whichever is lower.

See less