The correct answer is Option C. The Profit and loss statement is also referred to as the statement of revenues and expenses. It is because the Profit and Loss statement reports all types of revenue that have been earned and all types of expenses that have been incurred during a particular period ofRead more

The correct answer is Option C.

The Profit and loss statement is also referred to as the statement of revenues and expenses. It is because the Profit and Loss statement reports all types of revenue that have been earned and all types of expenses that have been incurred during a particular period of time.

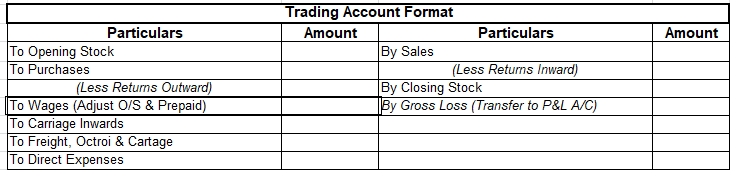

Option A Trading Account reports only the operating revenues and operating expenses.

Option B Trial Balance shows the balances of all the ledgers of a business and is prepared to check the arithmetical accuracy of the books of accounts.

Option D Balance sheet reports the balances of assets and liabilities of a business as at a particular date.

People often confuse the trading and the profit and loss statement to be the same. But they are different.

Trading Account is prepared with aim of arriving at operating profit or gross profit whereas the profit and loss statement is prepared to arrive at the net profit of a business and reports every revenue and expense whether operating or non operating in nature.

Operating revenue and operating expense are earned or incurred respectively are related to the chief business activities of a business.

Features of profit and loss statement:

- It is prepared to measure the net profit of a business hence its profitability.

- It is usually prepared for a period of one year but many companies do prepare quarterly statements to better judge their performance.

- It helps the management in decision making and the other stakeholders like shareholders, creditors to make informed decisions.

Sundry Debtors Sundry Debtors are those persons or firms to whom goods have been sold or services rendered on credit and the payment has not been received from them. In other words, Debtors are the persons or firms from whom the payment is to be received by the business. For Example, Ramen Sold goodRead more

Sundry Debtors

Sundry Debtors are those persons or firms to whom goods have been sold or services rendered on credit and the payment has not been received from them. In other words, Debtors are the persons or firms from whom the payment is to be received by the business.

For Example, Ramen Sold goods to Sam on credit, Sam did not pay for the goods immediately, so here Sam is the debtor for Ramen because he owes the amount to Ramen.

Another Example, If goods worth Rs 7000 have been sold to Sid on credit, he will continue to remain as debtor of the business so long as he does not make the full payment.

Treatment:

Sundry Debtor is considered as a current asset and hence it is shown on the assets side of the balance sheet under the Current Assets heading.

Sundry Debtors are not considered as an item of profit and loss because it is not considered as an item of income or expense. However, the items associated with sundry debtors such as bad debts or provision for doubtful debts or bad debts recovered are shown in profit and loss accounts in the debit and credit sides respectively.

Sundry Creditors

Sundry creditors are those persons or firms from whom goods have been purchased or services rendered on credit and for which payment has not been made. In other words, Creditors are the person or firms to whom some money has to be paid by the business.

For Example, Ramen purchased goods from Sam on credit, Ramen did not pay for the goods immediately, so here Ramen is the creditor for Sam because he owes money to Sam.

Another Example, If Mr. Johnson purchased goods worth Rs 3000 from M/s. Rick & Co. on credit, Mr. Johnson will continue to remain as a creditor of M/s. Rick & Co. as long as the full payment is made by Mr. Johnson.

Treatment:

Sundry Creditor is shown in the liabilities side of the balance sheet under the heading Current Liabilities.

See less