No, the building is not a current asset. Explanation Current assets are those in a business that is reasonably expected to be sold, consumed, cashed, or exhausted within one year of accounting through normal day-to-day business operations. Examples: Cash and cash equivalent, stock, liquid assets, etRead more

No, the building is not a current asset.

Explanation

Current assets are those in a business that is reasonably expected to be sold, consumed, cashed, or exhausted within one year of accounting through normal day-to-day business operations.

Examples: Cash and cash equivalent, stock, liquid assets, etc.

The building is expected to have a valuable life for more than a year and is bought for a longer term by a company. The building is a fixed asset/non-current asset, those assets which are bought by the company for a long term and aren’t supposed to be consumed within just one accounting year.

In order to understand it more clearly, let’s see the two types of assets in the classification of the assets on the basis of convertibility:

In the classification of the assets on the basis of their convertibility, they are classified either as current assets or fixed assets. Also referred to as current assets/ non-current assets or short-term/ long-term assets.

- Current Assets – As explained above, those assets in a business that is reasonably expected to be sold, consumed, cashed, or exhausted within one year of accounting.

- Fixed Assets – Those assets which are not likely to be converted into cash quickly and are bought by the business for a long term.

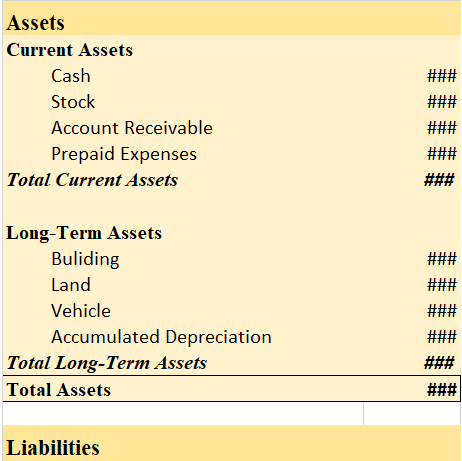

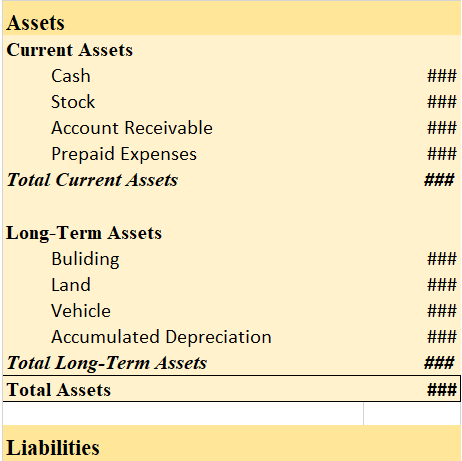

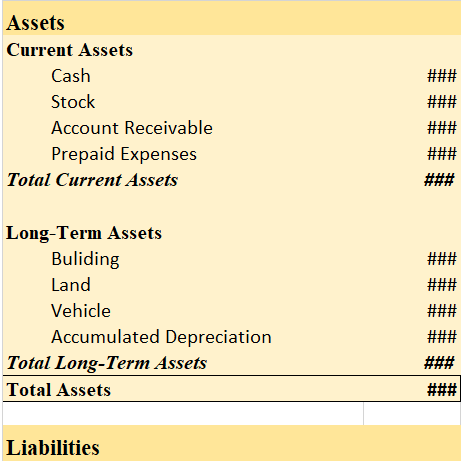

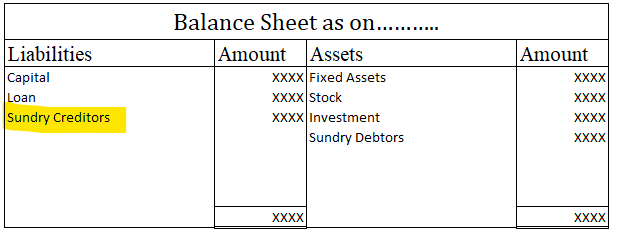

Building in the balance sheet

Let us take a look at the balance sheet’s asset side and see where building and current assets are shown

Balance Sheet (for the year ending…)

As we can see, the building is shown on the long-term assets side and not in the current assets.

Therefore, the building is not a current asset.

See less

Journal entries in the ledger What is a Journal Entry? Journal entry is a form of bookkeeping. All the economic or non-economic transactions in the business are recorded in the journal entries showing a company's debit or credit balances. It is a double-entry accounting method and requires at leastRead more

Journal entries in the ledger

What is a Journal Entry?

Journal entry is a form of bookkeeping. All the economic or non-economic transactions in the business are recorded in the journal entries showing a company’s debit or credit balances. It is a double-entry accounting method and requires at least two accounts or more in a transaction.

The journal entry helps to identify the transactions. We use journals to get a running list of business transactions. Each journal entry provides this specific information about a transaction:

General Ledger

After the transactions are recorded in the journal, they are posted in the principal book called ‘Ledger’. A ledger account contains information about a specific account. It contains the opening balance as well as the closing balances of an account. It summarizes the business transactions.

Transferring the entries from journals to respective ledger accounts is called ledger posting or posting to the ledger accounts. Balancing of ledgers is carried out to find differences at the year’s end, it means finding the difference between the debit and credit amounts of a particular account.

For instance,

Suppose goods were bought for cash. While passing the journal entry, we’ll be debiting the purchases a/c and crediting the cash a/c by stating it as, ‘To Cash A/c’.

Now, this entry will be affecting both the purchases account and the cash account. In the cash account, we’ll be debiting purchases. Whereas in the purchases account, we’ll be crediting the cash. That’s how it works in the double-entry bookkeeping system of accounting.

Example

Mr. Tony Stark started the business with cash of $100,000. He bought furniture for business for $15,000. He further purchased goods for $75,000. He hired an employee and paid him a salary of $5,000.

Now, we’ll be journalizing the transactions and posting them into the ledger accounts.

Journal Entries

Recording into Ledger Account

Cash A/c

Capital A/c

Furniture A/c

Purchases A/c

Salary A/c

Note: The balance b/d is not applicable as this is the business’ commencement year.

See less