To begin with, lets us understand what the Companies Act 2013 tells about calls-in-advance, so basically as per section 50 of the companies act 2013 "A company may if so authorized by its articles, accepts from any members the whole or part of amount remaining unpaid on any share held by him, even iRead more

To begin with, lets us understand what the Companies Act 2013 tells about calls-in-advance, so basically as per section 50 of the companies act 2013 “A company may if so authorized by its articles, accepts from any members the whole or part of amount remaining unpaid on any share held by him, even if no amount has been called up”.

To be more precise whenever excess money is received by the company than, what has been called up is known as calls-in-advance.

Accounting Treatment

Well, it is to be noted that calls-in-advance is never a part of share capital. A company when authorized by its article can accept those advance amounts and directly credit the amount received to the calls-in-advance account.

As these advance amounts are a liability for the company these are shown under the head current liability of the balance sheet until calls are made and are paid to the shareholders.

Since this is the liability of the company, it is liable to pay the interest amount on such call money from the date of receipt until the payment is done to the shareholders. The rate of interest is mentioned in the articles of association. If the article is silent regarding the rate on which interest is paid then it is assumed to be @6%.

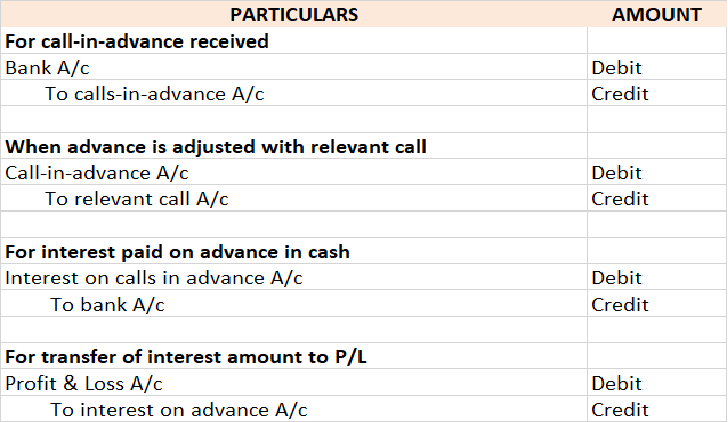

Accounting Entry

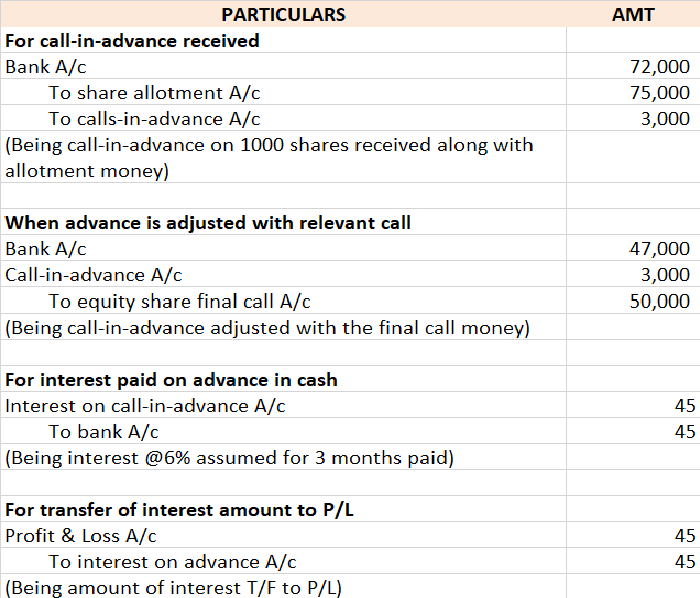

Bonnie let us understand the entries with help of an example

ADIDAS LTD issued 25,000 equity shares of Rs 10 each payable as follows:

ON APPLICATION Rs 5

ON ALLOTMENT Rs 3

ON FINAL CALL Rs 2

Application on 30,000 shares was received. excess money received on the application was refunded immediately. Mr. X who was allotted 1,000 shares paid the call money at the time of allotment and all amounts were duly received assume interest rate @6% for 3 months, so the relevant accounting entry goes as follows:

Important Points to be noted under calls-in-advance as per the companies act 2013

- The shareholder is not entitled to any voting rights on money paid until the said money is called for.

- No dividends are payable on advance money.

- Board may pay interest on advance not exceeding 12%.

- The shareholders are entitled to claim the interest amount as mentioned in the article, if there are no profits, then it must be paid out of capital because shareholders become the creditors of the company.

Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic lRead more

Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic life or service life

It is a useful concept in accounting as it is used to work out depreciation. By knowing this useful life of an asset an entity can easily analyze how to allot the initial cost of an asset across the relevant accounting period rather than doing it unfairly manner.

How do we calculate the useful life of an asset?

The useful life of an asset is not an accounting policy, but an accounting estimate. calculating useful life is not an exact phenomenon but an estimate that is done because it directly impacts how much an asset is to expense every year.

Factors affecting “how long an asset is expected to be useful” depends on some stated points as below:

As per the companies act 2013, some of the useful life of assets are stated below

To know more about the different categories of assets you can follow the given link useful life of assets.

POINT TO BE NOTED:- There lies a huge difference in the useful life v/s the physical life of an asset. It is very important to note that amount of time an asset is used in a business is not always be same as an asset’s entire life span.

See less