Meaning The term ‘Sundry creditors’ consist of two words: ‘Sundry’ and ‘creditors’. The word ‘sundry’ means the items which are not significant enough to be named separately. It also refers to a collection of miscellaneous items. Creditors are the person from whom money is borrowed or goods are puRead more

Meaning

The term ‘Sundry creditors’ consist of two words: ‘Sundry’ and ‘creditors’.

The word ‘sundry’ means the items which are not significant enough to be named separately. It also refers to a collection of miscellaneous items.

Creditors are the person from whom money is borrowed or goods are purchased on credit by a business or a non-business entity. They have to be repaid after a period of time which is usually less than or up to one year.

By combining the meaning of both words, ’sundry’ and ‘creditor’, the term ‘sundry creditor’ will refer to the collection of insignificant creditors of an entity.

Back in the days when accounting records were maintained on paper, only the records of those creditors were maintained separately, from whom goods are purchased regularly and in large amounts.

But there used to be numerous other creditors with whom the transactions were occasional and insignificant. To reduce the paperwork, records of all such creditors were maintained on a single page or book under the head ‘Sundry Creditors’

Nowadays, as accounting records are maintained digitally, hence maintaining records of each and every creditor is not a problem.

Hence, every creditor whether small or big, is grouped under the head ‘Sundry creditor’ or ‘Trade Creditor’.

Accounting Treatment

Sundry creditors are the persons to whom a business owes money.

Hence, as per golden rules of accounting, Sundry creditor is a personal account and the golden rule for personal account is, ‘Debit the receiver and credit the giver’

We know sundry creditors are liabilities, hence, as per modern rule of accounting, sundry creditors are credited in case of increase and debited in case of decrease.

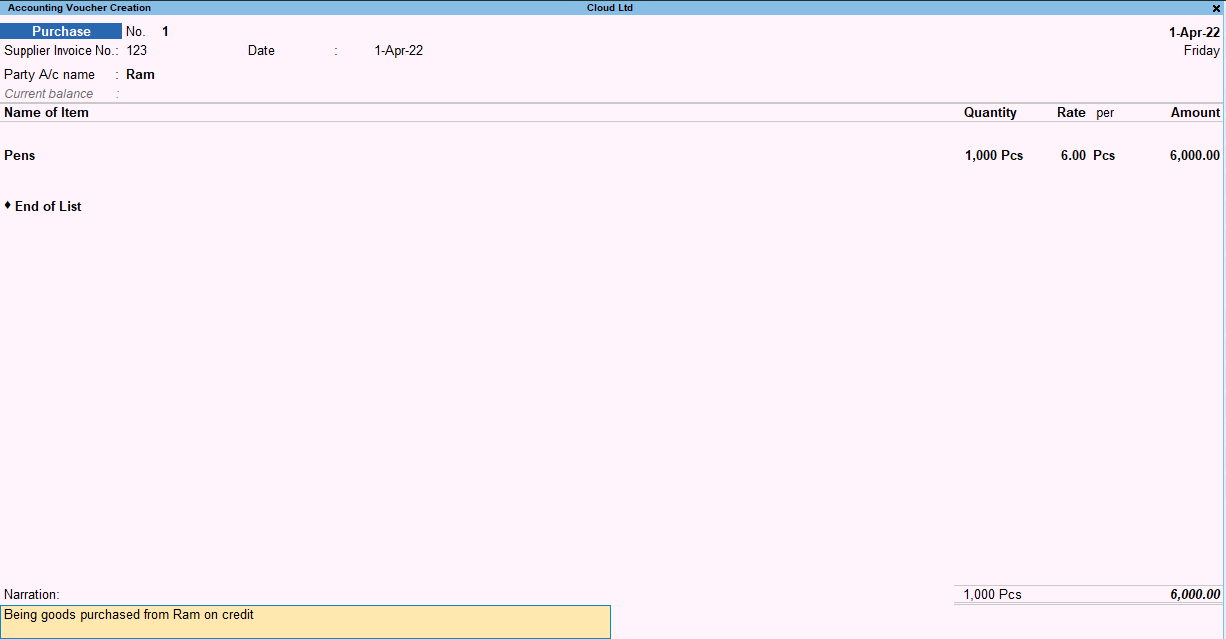

Example, a business purchased goods for Rs. 10,000 from ABC & Co. The journal entry will as follows:

Here, ABC & Co is the creditor. It is credited as it is a personal account and the creditor has given the goods to the business, hence the giver is credited.

From point of view of modern rules of accounting, ABC & Co. is a creditor, a liability. On purchase of goods on credit, a liability is created. Hence, ABC & Co A/c is credited.

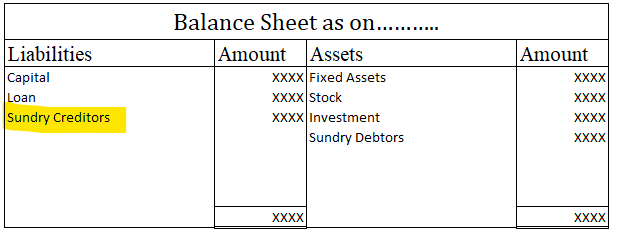

Balance sheet

Sundry creditor is a current liability, so it is shown on the liabilities side of a balance sheet. Trade payable and accounts payable mean sundry creditors only.

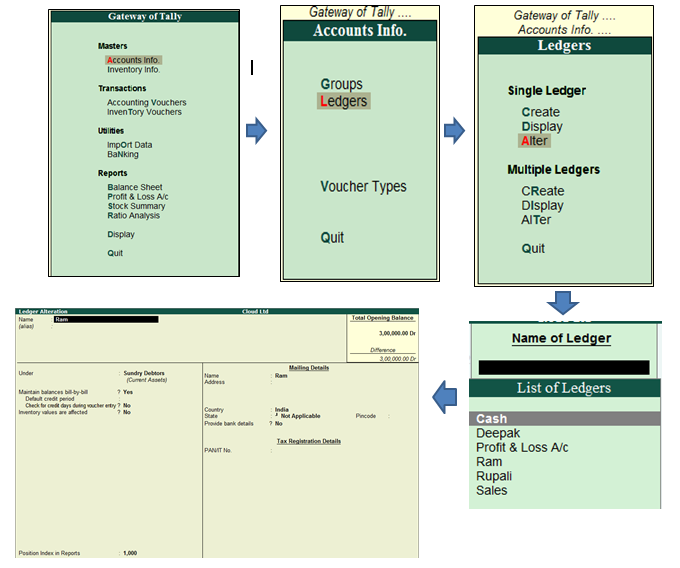

Ledger Folio A ledger folio, in simple words, is a page number of the ledger account where the relevant account appears. The term 'folio' refers to a book, particularly a book with large sheets of paper. In accounting, it's used to maintain ledger accounts. The use of ledger folio is generally seenRead more

Ledger Folio

A ledger folio, in simple words, is a page number of the ledger account where the relevant account appears. The term ‘folio’ refers to a book, particularly a book with large sheets of paper. In accounting, it’s used to maintain ledger accounts.

The use of ledger folio is generally seen in manual accounting, i.e the traditional book and paper accounting as it is a convenient tool used for tracking the relevant ledger account from its journal entry. Whereas, in computer-oriented accounting (or computerized accounting), it’s not really an issue to track your relevant ledger account.

Ledger folio, abbreviated as ‘L.F.’, is typically seen in journal entries. The ledger folio is written in the journal entries, after the ‘date’ and ‘particulars’ columns. It is really convenient when we’re dealing with and recording a large number of journal entries. As we will be further posting them into ledger accounts, thus, ledger folio comes in as a really useful component of journal entries.

Example

We’ll look at how the ledger folio column is used while recording journal entries.

We can find the relevant ledger accounts on the page numbers of the book as mentioned in the above entries, i.e. the cash and sales account on page – 1 whereas, the purchases and sundry creditors on page – 2 of the relevant ledger book.

See less