To understand why we do not record self-generated goodwill in accounting, let us first understand what goodwill is and its accounting treatment. What is Goodwill? Goodwill is an intangible asset of a business. It represents the reputation and brand value of a business built over time. It is a valueRead more

To understand why we do not record self-generated goodwill in accounting, let us first understand what goodwill is and its accounting treatment.

What is Goodwill?

Goodwill is an intangible asset of a business. It represents the reputation and brand value of a business built over time. It is a value over and above the tangible assets of the business.

Goodwill often arises when a business purchases another business and pays a premium, which means a price higher than the fair value of the business.

Characteristics of Goodwill

Goodwill has the following characteristics:

- It is an Intangible asset, meaning it has no physical existence and cannot be seen or touched.

- It is generally recognized during transactions in mergers and acquisitions.

- It is the value attributed to the brand value and reputation of the business.

- It adds value to a business beyond its tangible assets.

Example of Goodwill

Let us take an example to understand the concept of goodwill better.

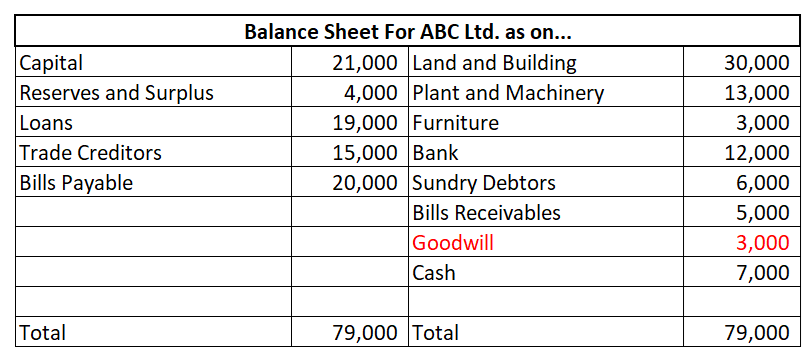

Suppose there is a company ABC Ltd. It is planning to acquire XYZ Ltd. The fair value of the assets of XYZ is calculated to be 600,000. However, ABC has agreed to pay a sum of 650,000 to acquire the company. This difference of 50,000 is goodwill.

Impact on Financial Statements

Goodwill is shown under the assets side of the Balance Sheet.

What is self-generated goodwill?

Self-generated goodwill in simple words means the positive reputation or trust that a business earns over time through their own hard work and decisions. It’s not something bought or inherited but something built from scratch internally, like a brand’s reputation, loyal customers, strong relationships, or unique ideas.

For example, a small business that goes the extra mile to offer great customer service or always delivers high-quality products over the years will naturally build goodwill.

It is also known as internally generated goodwill.

Why do we not record sef-generated goodwill?

Self-generated goodwill is not recorded in the financial statements because of the following reasons:

- Measurement may not be reliable: The measurement of self-generated goodwill is majorly based on the judgment of the managers. It is based on the value creation because of a good reputation or consumer base of the business, which might not be measured accurately.

- Conservatism principle: As per the conservatism principle, a business shall not overstate its assets or liabilities. However, self-generated goodwill might be overstated.

- Lack of market transaction: There is a lack of a market transaction that ensures verification of the value of goodwill as in the case of purchased goodwill.

- Manipulation: There are higher chances of manipulation of financial statements through self-generated goodwill.

Conclusion

On a concluding note, self-generated goodwill is something that adds real value to a business, but it’s not something that can easily be measured or captured in financial statements. Accounting is all about providing clear, reliable information, and including goodwill would make things murky and open to manipulation. Even though it doesn’t show up on the books, you can still see its effects in a company’s reputation and success. Maybe in the future, businesses will find a way to highlight it better, but for now, leaving it out helps keep financial reports honest and straightforward.

See less

Definition Gross profit is the excess of the proceeds of goods and services rendered during a period over their cost, before taking into account administration, selling, distribution, and financial expenses. When the result of this computation is negative it is referred to as gross loss Formula : ToRead more

Definition

Gross profit is the excess of the proceeds of goods and services rendered during a period over their cost, before taking into account administration, selling, distribution, and financial expenses.

When the result of this computation is negative it is referred to as gross loss

Formula :

Total Revenues – Cost Of Goods Sold

Net profit is defined as the excess of revenues over expenses during a particular period.

When the result of this computation is negative it is called a net loss.

Net profit may be shown before or after tax.

Formula :

Total Revenues – Expenses

Or

Total Revenues – Total Cost ( Implicit And Explicit Cost )

The basic difference between gross profit and net profit is that gross profit estimates the profitability of a company whereas net profit is to show the performance of the company.

Key points of Gross Profit

Some of the key points of as for gross profits follows :

• Stage of calculation: Gross Profit is calculated in the first stage of the Final Account.

• Purpose of calculation: It is calculated to know the total profit earned during the particular accounting

• Type of balance: Gross Profit shows the credit balance of the Trading Account.

• Dimension: It is a narrow concept as it is a part of Net Profit.

• Treatment: It is not treated directly in the balance sheet. It is transferred to the Profit And Loss Account.

Key points of Net Profit

Some of the key points of as for gross profits follows :

• Stage of calculation: Net Profit is calculated in the second stage of the Final Account.

• Purpose of calculation: It is calculated to know the net profit earned during the particular accounting

• Type of balance: Net Profit shows the credit balance of the Profit And Loss Account.

• Dimension: It is a wider concept as it includes Gross Profit.

• Treatment: It is treated directly in the balance sheet by adding or subtracting from the capital.

Examples

Now let me explain to you by taking an example which is as follows :

In a business organization there were the following data given as purchases made Rs 73000, inventory, in the beginning, was Rs 10000, direct expenses made were Rs 7000, closing inventory which was Rs 5000, revenue from operation during the period was Rs 100000.

Then,

COST OF GOODS SOLD = Purchases + Opening Inventory + Direct Expenses – Closing Inventory.

= Rs ( 73000 + 10000+ 7000- 5000)

= Rs 85000

GROSS PROFIT = REVENUE – COST OF GOODS SOLD

= Rs ( 100000 – 85000 )

= Rs 15000

Now from the above question keeping the gross profit same if the indirect expenses of the organization are Rs 2000 and the other income is Rs 1000.

Then,

NET PROFIT = GROSS PROFIT – INDIRECT EXPENSES + OTHER INCOMES

= Rs ( 15000 – 2000 + 1000)

= Rs 14000

Conclusion

So here I conclude that gross profit is the difference between revenues from sales and/or services rendered and its direct cost.

Whereas net profit is after the deduction of total expenses from the total revenues of the enterprise.

See less