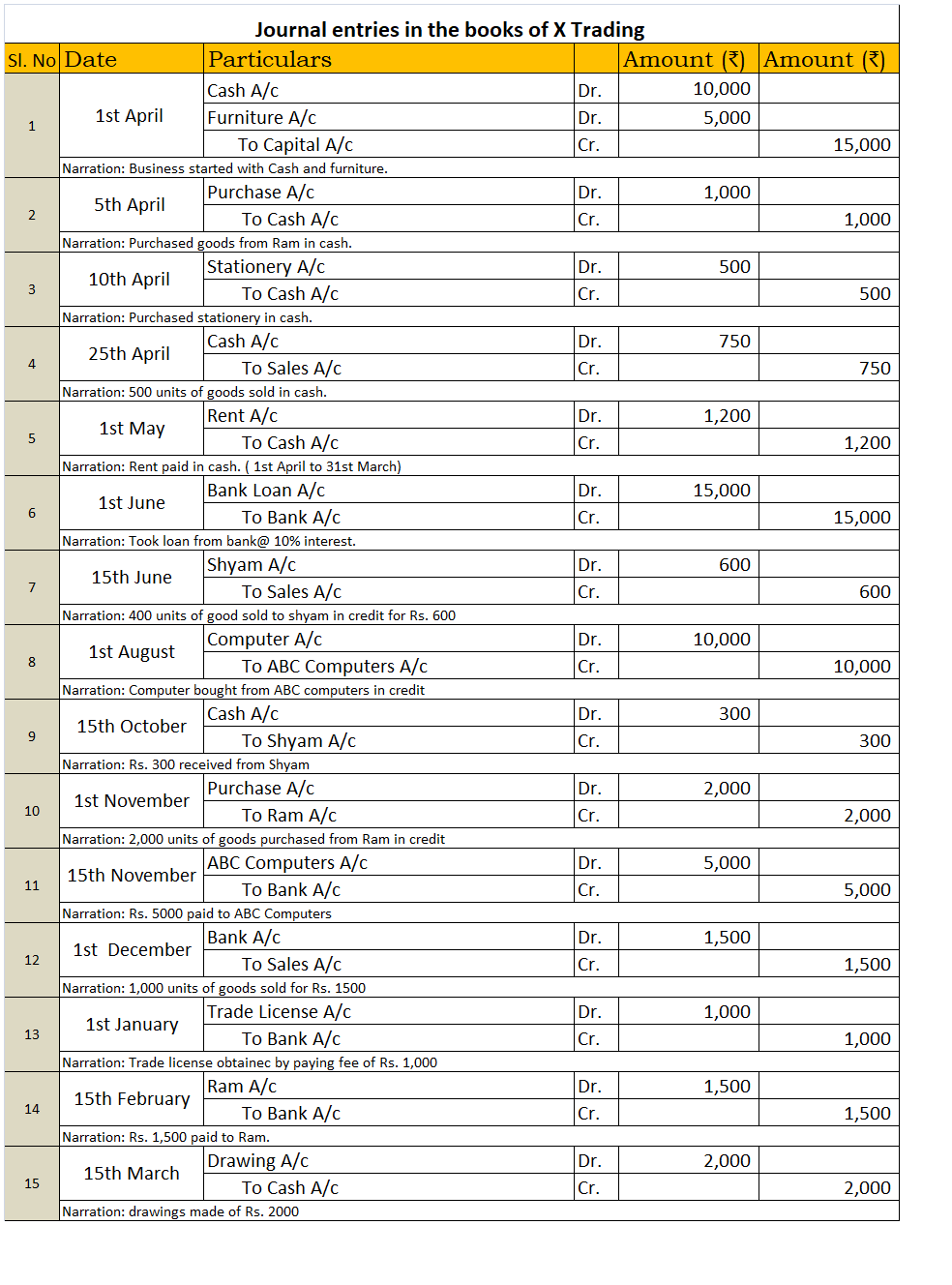

Let the business in our example be X Trading. The 15 transactions are as follows: 1st April - X Trading started its business with Rs. 10,000 cash and furniture of Rs. 5,000. 5th April - Purchased 1,000 units of goods for Rs. 1,000 in cash from Ram. 10th April – Bought stationery for Rs. 100 in cash.Read more

Let the business in our example be X Trading. The 15 transactions are as follows:

- 1st April – X Trading started its business with Rs. 10,000 cash and furniture of Rs. 5,000.

- 5th April – Purchased 1,000 units of goods for Rs. 1,000 in cash from Ram.

- 10th April – Bought stationery for Rs. 100 in cash.

- 25Th April – Sold 500 goods for Rs. 750 in cash.

- 1st May – Paid a rent of Rs. 1200 ( 1st April to 31st March)

- 1st June – Took a loan of Rs. 15,000 from the bank at interest@10%.

- 15Th June – Sold 400 goods for Rs. 600 to Shyam in credit.

- 1st August – Bought a computer for Rs. 10,000 in from ABC Computers in credit.

- 15th October – Received Rs. 300 from Shyam in cash.

- 1st November – Purchased 2,000 units of goods for 2,000 from Ram in credit.

- 15th November – Paid Rs. 5,000 to ABC Computers through cheque.

- 1st December – Sold 1,000 units of goods for Rs. 1,500. Received cheque as payment.

- 1st January – Obtained Trade license (valid for 5 years) by paying fees of Rs. 1000 through online bank transfer.

- 15Th February – Paid Rs. 1,500 to Ram. Through cheque.

- 15Th March – Drawings made of Rs. 2000 in cash.

We will prepare the journal, ledgers and the trial balance from the above transactions.

Journal

Journal is known as the book of primary entry or book of original entry. It is because every transaction is recorded in form of journal entries in the journal. Every journal entry affects at least two accounts (dual effect). A transaction has to be a monetary transaction otherwise it cannot be recorded as a journal entry.

The procedure of recording transactions as journal entries is simple if we follow the modern rules of accounting.

So first we have to identify which and what type of account does a transaction affect. The types of accounts are:

- Asset – Debit in case of increase Credit in case of decrease.

- Liabilities – Debit in case of decrease Credit in case of increase.

- Capital – Debit in case of decrease Credit in case of increase.

- Expense – Debit in case of increase Credit in case of decrease.

- Income – Debit in case of decrease Credit in case of increase.

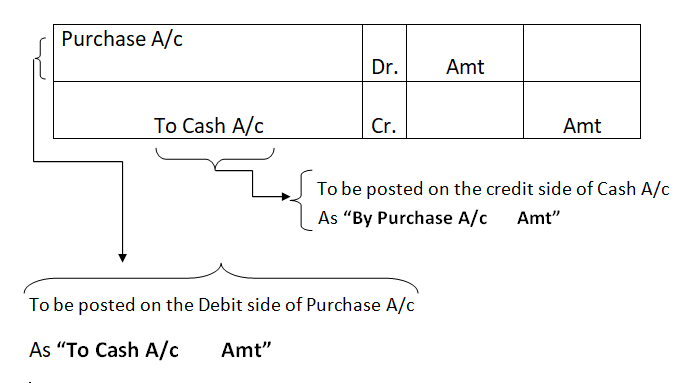

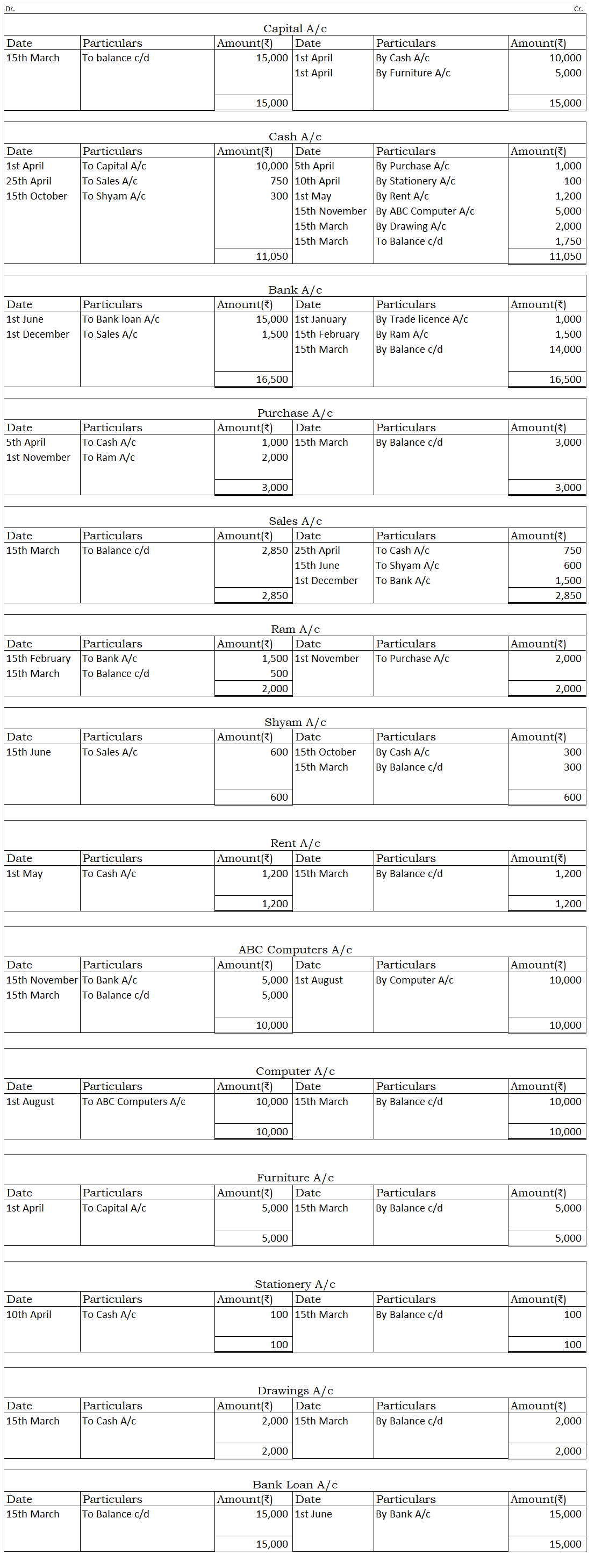

Ledger

Ledgers are known as the books of principal entry or book of final entry. All the journal entries recorded in the journal are posted to the ledgers. A Ledger is where the entries related to a particular account are recorded. For example, all the transactions related to salary will be recorded in the salary account ledger.

It is very important to prepare the ledger to arrive at the balance of each account in the books of concern so that it can prepare its trial balance.

The procedure of posting journal entries in the ledger account is done is as follows:

The ledgers are as follows:

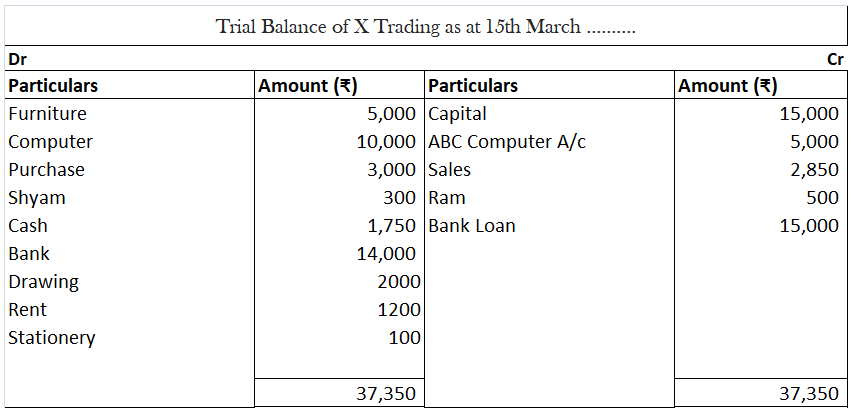

Trial Balance

The trial balance is not a part of the books of accounts. It is just a statement prepared to check the arithmetical accuracy of the books of the accounts. It also helps to know about the omission and posting mistakes. It is prepared after the ledger accounts have been drawn and their balances have been ascertained.

The balance of all the ledger accounts is posted on either side of the trial balance. Debit balance of the account on the debit side and credit balance of the account on the credit side.

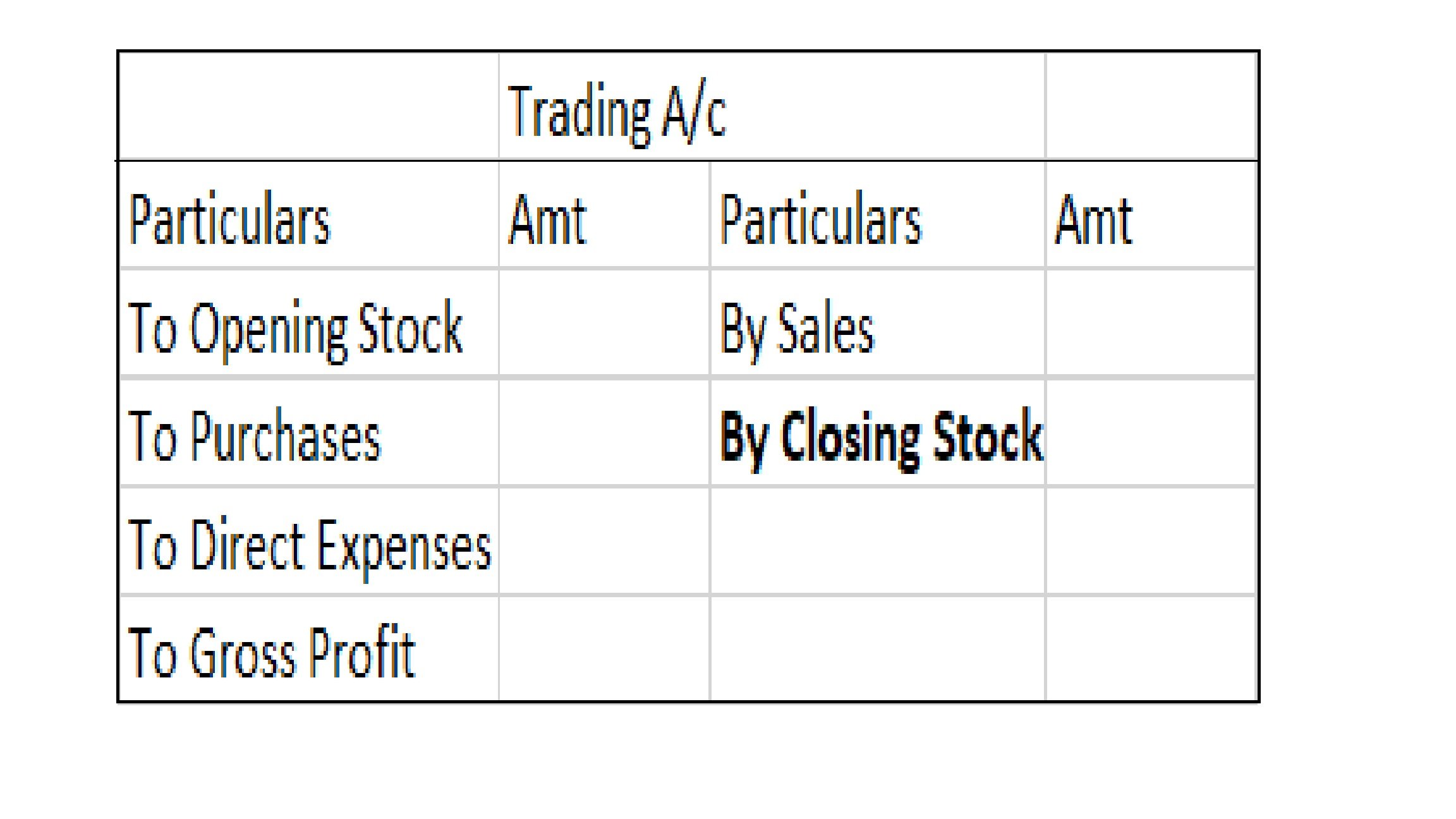

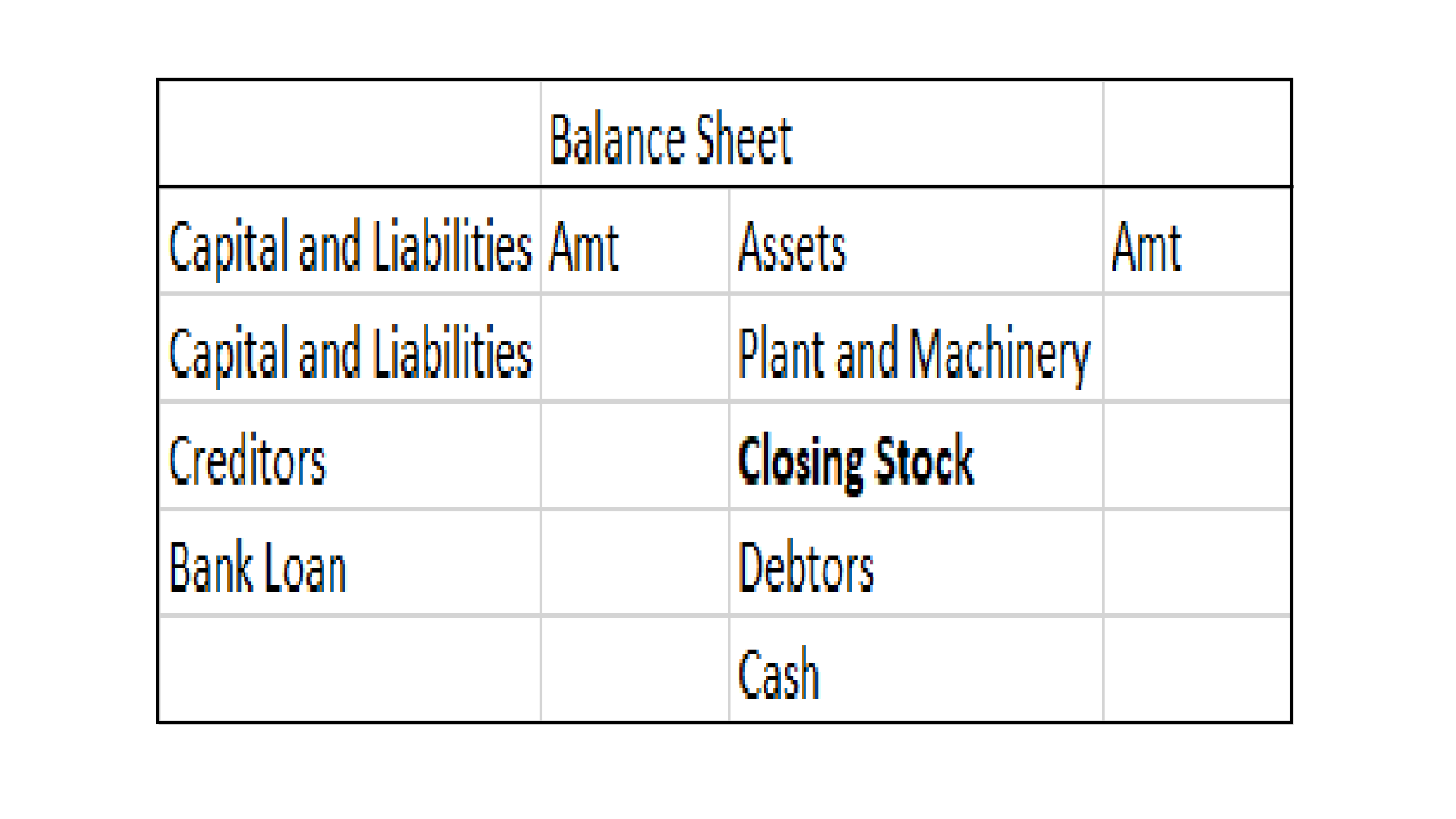

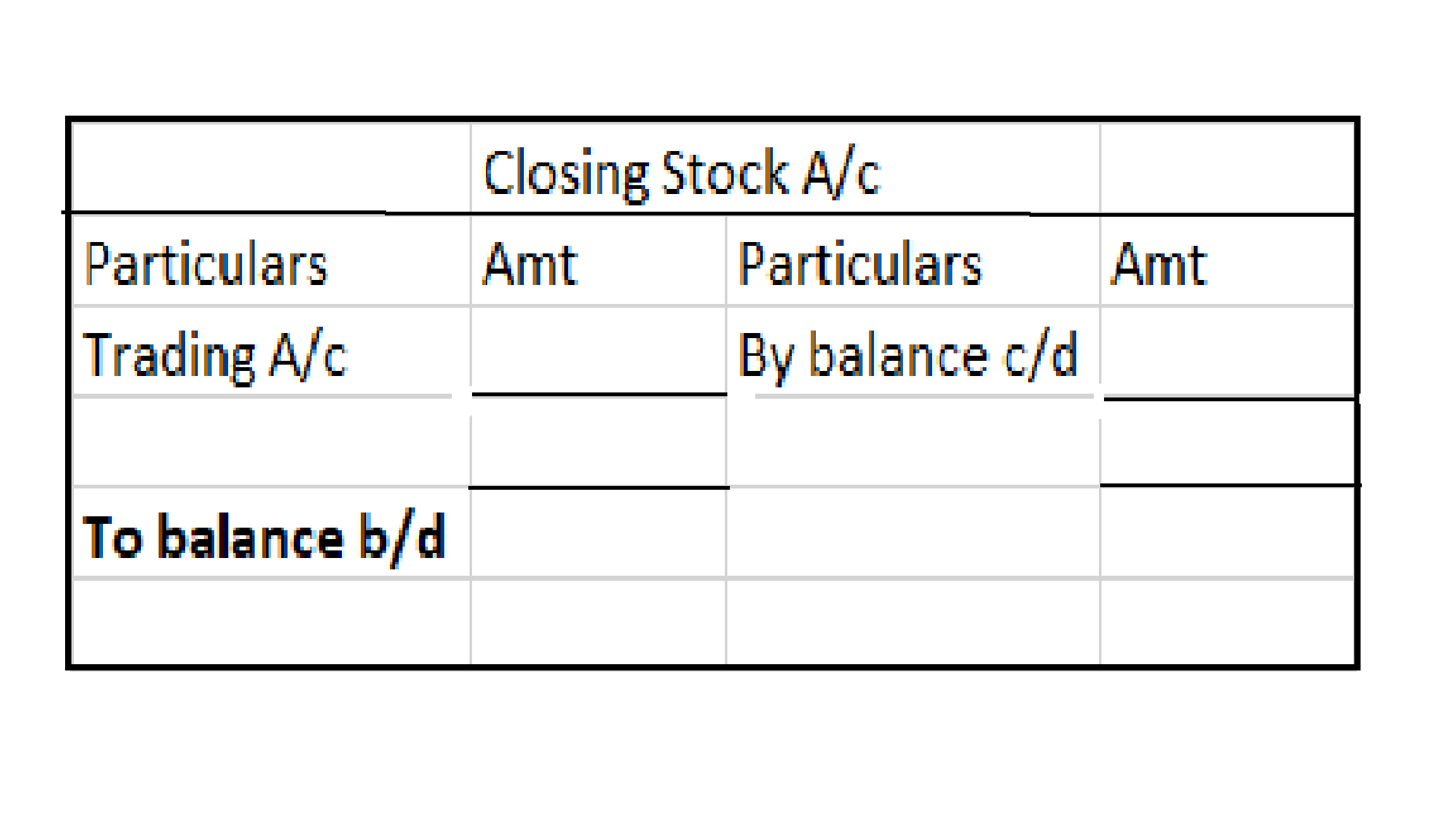

Also, the closing stock from the financial statements of the previous year is posted on the debit side of the trial balance as opening stock to account for the stock with the business at the beginning of the financial year.

Following is the trial balance of X trading:

Fictitious assets On seeing or hearing ‘fictitious’, the words which come to our mind are ‘not true, ‘fake’ or ‘fantasy’. So, fictitious assets are those items that appear on the assets side of the balance sheet but are actually not assets. In substance, fictitious assets are the expenses and lossesRead more

Fictitious assets

On seeing or hearing ‘fictitious’, the words which come to our mind are ‘not true, ‘fake’ or ‘fantasy’. So, fictitious assets are those items that appear on the assets side of the balance sheet but are actually not assets.

In substance, fictitious assets are the expenses and losses that are not completely written off in a financial year and are required to be carried forward to the next financial year.

The examples of fictitious assets are as follows:

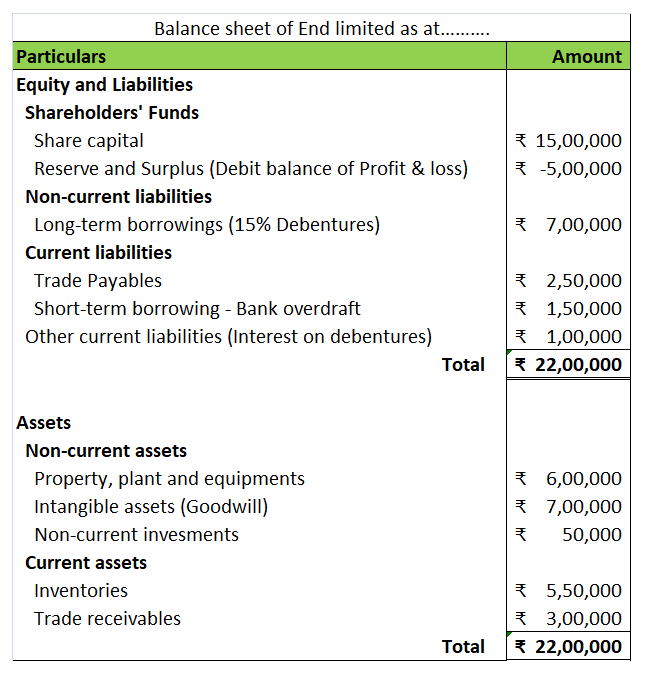

Fictitious assets appear on the asset side of the balance sheet as expenses and losses have a debit balance.

*when the balance sheet is prepared as per Schedule III of Companies Act, the Net loss is shown as a negative figure under the head Reserve and Surplus.

Intangible Assets

Intangible assets mean the assets which don’t have any physical existence. They cannot be seen or touched but are assets because they do provide future economic benefits to the business. Like tangible assets (like machinery and building), they can be also created, purchased or sold.

Like tangible assets are depreciated, intangible assets are gradually written over by amortization over their useful lifespan to account for the economic benefits provided by them.

Following are the examples of intangible assets:

Intangible assets which are created by the business-like goodwill or brand recognition do not appear in the balance sheet.

Only acquired intangible assets can be shown in the balance sheet. Like purchased goodwill, patents, trademarks etc.

Intangible assets also face impairment if their fair value is less than their carrying value after deducting amortization expense. The difference between carrying value and fair value is shown in the Profit and loss A/c as impairment charge and the asset is valued at fair value in the balance sheet.

See less