The term ‘contra’ means opposite or against. In financial accounting, we encounter the term ‘contra’ in: Contra accounts Contra entries The meaning of contra in the above mention terms is also the same as their general meaning. Contra accounts mean the account which is opposite of the account it corRead more

The term ‘contra’ means opposite or against. In financial accounting, we encounter the term ‘contra’ in:

- Contra accounts

- Contra entries

The meaning of contra in the above mention terms is also the same as their general meaning. Contra accounts mean the account which is opposite of the account it corresponds to.

Contra entries are entries of the debit and credit aspects related to the same parent account. Let’s discuss them in detail.

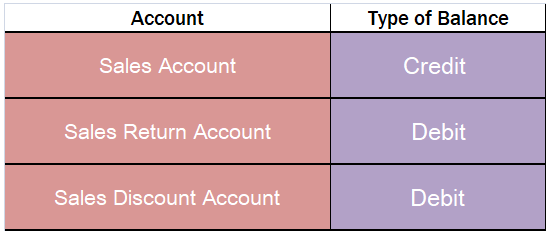

Contra accounts

Any account which is created with the purpose of reducing or offsetting the balance of another account is known as a contra account.

A contra account is just the opposite of the account to which it relates. The most common examples are the sales discount account and sales return account which is the contra account of the sales account. They are just the opposite of the sales accounts.

Contra Entries

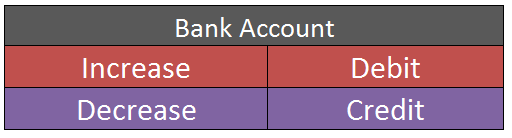

Contra entries refer to the entries which show the movement of the amount within the same parent account. Here, the debit and credit entry is posted on the debit and credit side respectively of a single parent account. Mainly, contra entries are the entries involving cash and bank accounts.

The following transactions are recorded as contra entries:

- Cash to Bank transactions: Deposit of cash into the bank account by the entity.

- Bank to Cash transactions: Withdrawal of cash from the bank.

- Cash to cash transactions: Transfer of cash to the petty cash account.

- Bank to Bank transactions: Transfer of amounts from one bank account to other bank accounts of the same entity.

Contra entries are marked by the letter ‘C’ beside the postings in the ledger. Deposit of cash in to bank will be posted in cashbook as below:

When a loan is taken from a person by a business, there is an asset and liability being created. Cash is being brought into the business which increases the asset whereas the financial obligation of the company rises when a loan is taken and hence a liability increases. For example, Mark Ltd. has taRead more

When a loan is taken from a person by a business, there is an asset and liability being created. Cash is being brought into the business which increases the asset whereas the financial obligation of the company rises when a loan is taken and hence a liability increases.

For example, Mark Ltd. has taken a loan from John for $5,000. Therefore the journal entry can be shown as:

According to the modern rules of accounting, increase in assets is Debit and increase in liability is credit. The company may have taken the loan to finance its business or for some emergency. When it is time for the business to pay off the loan, they can either pay it off completely or in instalments. They must pay off the principal amount along with interest.

Now for our above example, if Mark Ltd paid off the entire loan after one year at 10% interest, then the journal entry would be:

Here, the interest on loan account is debited since an increase in expense is debited. Loan account will be debited because the obligation is now reduced and hence liability decreases. Finally, we credit cash since cash is leaving the business which implies a decrease in assets.

If the entire loan is not paid off in that year, then the balance of the loan amount will be shown in the balance sheet under the head liabilities.

See less