Consignment is "goods sent by its owners to his agent for the purpose of sale". In simple language, the word consignment means to send goods to another person for sale on his behalf without transfer of ownership. In accounting terms, consignment is the process where the owner (consignor) transfers tRead more

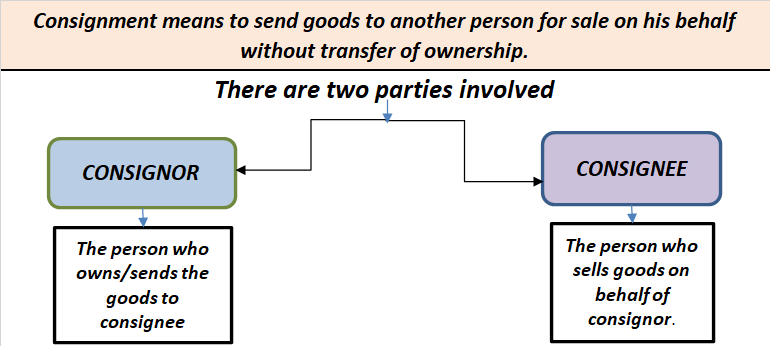

Consignment is “goods sent by its owners to his agent for the purpose of sale”. In simple language, the word consignment means to send goods to another person for sale on his behalf without transfer of ownership.

In accounting terms, consignment is the process where the owner (consignor) transfers the possession of the goods to the agent (consignee) to make a sale on his behalf while the ownership of goods remains with the owner until the sale is made by the agent. In return, the agent receives an agreed percentage of the sum in the form of commission.

Generally, there are two parties involved in consignment, those are as follows:

- CONSIGNOR: the person who is the owner and sender of goods.

- CONSIGNEE: the person who receives goods for sale/resale from the consignor in exchange for a percentage of the sale or on an agreed sum known as commission.

The relationship between consignor and consignee is that of principal and agent.

Let me give you a simple example of how consignment works.

Mr. John (consignor) sends goods to Mr. Jeh (consignee) worth Rs 20,000 to sell these goods at a cost plus 10%. Mr. Jeh agrees to sell these goods on his behalf for a commission of 1% on the sale. Therefore Mr. Jeh sold these goods at the agreed amount i.e Rs 22,000 [20,000+ 10% of 20,000] and charges Rs 220 [1% of Rs 22,000] as commission made on such sale and remit the remaining balance to the owner Mr. John.

There is a lot of confusion regarding “is consignment the same as the sale of goods?“. The answer is NO.

The reason what makes it different from the sale is

a) In sale the ownership gets transferred from seller to buyer but in case of consignment the ownership remains with the consignor until the sale is made by the agent.

b) In sale the risk gets transferred with the transfer of goods, whereas in consignment the risk remains with the owner till the sale is made.

c) Also goods once sold cannot be returned on damages /defaults, but in case of consignment goods that come to be faulty can be returned to the consignor.

Before starting with the main discussion, let me give you a brief explanation of what rent received is When a business or an organization rents out its unused property to earn some extra income and receive some amount from it, that amount of money is said to be rent received. Rent can be monthly, quRead more

Before starting with the main discussion, let me give you a brief explanation of what rent received is

When a business or an organization rents out its unused property to earn some extra income and receive some amount from it, that amount of money is said to be rent received.

Rent can be monthly, quarterly, half-yearly, or yearly rent depending upon the organization’s agreement.

The journal entry for rent received will be

Here, Cash account is debited due to the increase in assets or because of a real account. Rent account is credited due to the increase in income or because of the nominal account.

However, Rent received in advance means the amount of rent that is not yet due but is received in advance. It is treated as a current liability because the benefit related is yet to be provided to the tenant.

The Journal entry for Rent received in advance will be-

Here, rent is debited due to a decrease in income.

Rent received in Advance is credited due to an increase in liability.

For Example, Johnson company rented out a part of its building that was not used to earn some extra income from it. The monthly rent was fixed as 20000. Johnson company follows calendar year as their accounting year. The tenant, therefore, paid 4 months advance rent to Johnson company i.e. the tenant in January gave his advance rent for February, March, April, and May.

While receiving the rent in the month of January. The journal entry would be

Now, the adjustment entry of rent received in advance would be

The rent received in advance will also be posted individually in each month of February, March, April, and May as

Furthermore, Rent received in advance is deducted from the amount of rent in the income and expenditure account and thereafter the amount received in advance is posted on the liability side of the Balance sheet.

See less