Based on duration, expenses can be categorized as capital expenditure and revenue expenditure. A) Capital expenditure or CAPEX are those funds that are used to acquire or maintain or enhance long-term assets. Such expenses do not occur frequently and are incurred to enhance the company’s utility inRead more

Based on duration, expenses can be categorized as capital expenditure and revenue expenditure.

A) Capital expenditure or CAPEX are those funds that are used to acquire or maintain or enhance long-term assets. Such expenses do not occur frequently and are incurred to enhance the company’s utility in the long-term i.e. more than one year.

The formula of CAPEX can be given as –

Capital expenditure = Net increase in PP & E + Depreciation Expense

. It is showed in companies’ cash flow statement and in its Balance Sheet under the head of fixed assets. These capital expenditures are capitalized.

List of some capital expenses –

- Buildings (Including costs of purchase and other cost that extend the useful life of a building)

- Computer equipment (Cost of purchase and installation cost)

- Office equipment (Purchase cost)

- Furniture and fixtures (Cost of purchase and installation cost)

- Intangible assets (i.e. patent, trademark)

- Land (Including the cost of purchasing and upgrading the land)

- Machinery (Purchase cost and costs that bring the equipment to its location and for its intended use)

- Software (Installation cost)

- Vehicles

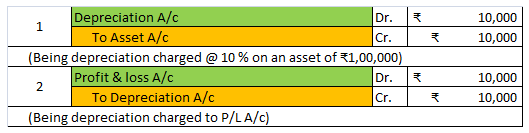

Example- If an asset costs Rs10,000 when bought and installation cost is Rs2000. The total capital expenditure will be Rs12000 and is expected to be in use for five years, Rs2,500 may be charged to depreciation in each year over the next five years.

B) Revenue expenditure or OPEX are those expenses that are incurred during its course of the operation. It can also be termed as total expenses that are incurred by firms through their production activities. Such costs do not result in asset creation, and the benefits resulting from it are limited to one accounting year. These are for managing operational activities and revenue within a given accounting period.

The accounting treatment for revenue expenditure for an accounting period is shown in a companies Income Statement, but it is not recorded in the firm’s Balance Sheet. OPEX is not capitalized and depreciation is not levied on such expenses.

Examples for revenue expenditures are as follows –

- Direct expenses

These types of expenses are mostly incurred directly through the production process. Common direct expenses include – direct wages, freight charge, rent, material cost, legal expenses, and electricity cost.

- Indirect expenses

These expenses are indirectly related to production like during sale, distribution, and management of finished goods or services. They include expenses like selling salaries, repairs, interest, commission, depreciation, rent, and taxes, among others.

See less

The word, “deferred” means delayed or postponed and “revenue” in layman’s terms means income. Therefore deferred revenue means the revenue which is yet to be recognised as income. It is actually unearned income. In accrual accounting, income is recognised only when it is accrued or earned. DeferredRead more

The word, “deferred” means delayed or postponed and “revenue” in layman’s terms means income. Therefore deferred revenue means the revenue which is yet to be recognised as income. It is actually unearned income.

In accrual accounting, income is recognised only when it is accrued or earned. Deferred revenue is the income received before the performance of the economic activity to earn it.

Example: A shoe shop owner gives an order to a shoe manufacturer of 1000 pair of shoes which is to be delivered after 4 months. He also gives him a cheque of ₹15,000 in advance, the rest ₹5000 is to be given at the time of delivery.

So, in this case, the ₹15,000 is actually is unearned revenue i.e. deferred revenue. It will be recognised as revenue when the shoe manufacture completes the order and deliver it.

Till then, the deferred revenue is reported as a liability in the balance sheet. Like this:

After recognition as revenue, it will be reported in the statement of profit or loss:

Hence, to summarise, deferred revenue is:

Some examples of deferred revenue are as follows:

Now the question arises why deferred revenue is recognised as a liability. It is due to the fact that the business may not be able to perform the economic activity successfully to earn that revenue.

Taking the above example, suppose the shoe manufacturer is not able to honour its commitment and the shoe shop owner can wait no more, then the advanced money of ₹ 15,000 is to be refunded. That’s why deferred revenue is recognised as a liability because it is a liability if we consider the principle of conservatism (GAAP).

See less