Receipts Amount Payments Amount To Balance b/d 32,500 By Salaries 31,500 To Subscription By Postage 1,250 2016-17 1,500 By Rent 9,000 2017-18 60,000 By Printing and 2018-19 1,800 63,300 Stationery 14,000 To Donations (Billiards Table) 90,000 By Sports Material 11,500 By Miscellaneous Expenses 3,100 To Entrance Fees 1,100 By Furniture (1.10.2017) 20,000 To Sale of old magazines 450 By 10% investment (1.10.2017) 70,000 By Balance ...

In the books of Krish Fitness and Wellness Club Income & Expenditure A/c for the year ended 31 March 2020 Expenditure Amt Income Amt To Doctors and Coaches Honorarium 25,000 By Subscription (600*100) 60,000 To Medicines 15,500 By Entrance Fees 25,000 To General Expenses 8,000 By Miscellaneous ReRead more

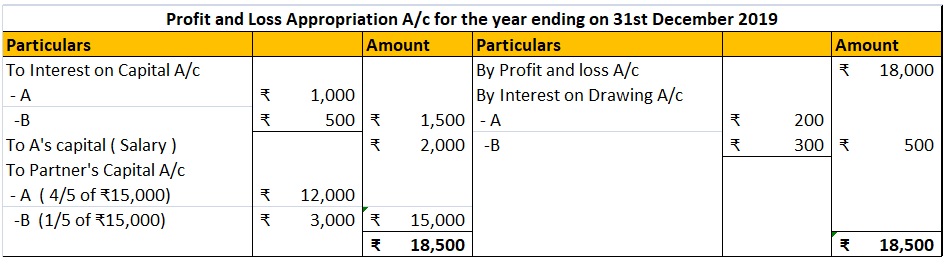

In the books of Krish Fitness and Wellness Club

Income & Expenditure A/c for the year ended 31 March 2020

| Expenditure | Amt | Income | Amt |

| To Doctors and Coaches Honorarium | 25,000 | By Subscription (600*100) | 60,000 |

| To Medicines | 15,500 | By Entrance Fees | 25,000 |

| To General Expenses | 8,000 | By Miscellaneous Receipts | 15,000 |

| To Newspaper | 8,000 | By Deficit (excess of expenditure over income) | 21,500 |

| To Rent, Rates and Taxes | 5,000 | ||

| To Tournament Expenses (W.N.1) | 25,000 | ||

| To Loss on Sale of Medical Equipment (W.N.2) | 10,000 | ||

| To Depreciation on Medical Equipment | 25,000 | ||

| 1,21,500 | 1,21,500 |

Working Notes:

1.Calculation of Tournament Fund

| Tournament Fund as of 1 April 2019 | 15,000 |

| Add: Donations to Tournament Fund | 20,000 |

| Less: Tournament Expenses | -60,000 |

| Tournament Expenses | -25,000 |

2. Calculation of Loss on Sale of Medical Equipment

| Book Value of Medical Equipment | 15,000 |

| Less: Sold | -5,000 |

| Loss on Sale of Medical Equipment | 10,000 |

In the books of Youth Ltd. Income & Expenditure A/c for the year ended 31 March 2018 Expenditure Amt (₹) Income Amt (₹) To Salaries 31,500 By Subscription (W.N.1) 75,000 To Postage 1,250 By Entrance fees 1,100 To Rent 9,000 By Sale of old magazines 450 To Printing and Stationery 14,000 By IntereRead more

In the books of Youth Ltd.

Income & Expenditure A/c for the year ended 31 March 2018

Working Notes:

See less