Introduction A capital reduction account is an account used to pass entries related to the internal reconstruction of a company. During reconstruction, paid-up capital reduced is credited to this account; hence its name is capital reduction account. It is also known as the reconstruction account. TyRead more

Introduction

A capital reduction account is an account used to pass entries related to the internal reconstruction of a company. During reconstruction, paid-up capital reduced is credited to this account; hence its name is capital reduction account. It is also known as the reconstruction account.

Type of account

A capital reduction account is a temporary account open just to carry out internal reconstruction. It represents the sacrifices made by the shareholders, debenture holders and creditors. Also, any appreciation in the value of assets is credited to this account. It is closed to capital reduction when internal reconstruction is completed.

Entries passed through capital reduction account

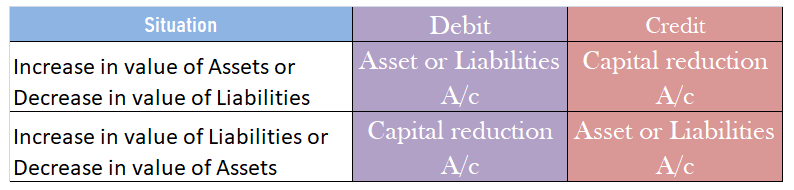

When paid-up capital is cancelled.

When paid-up capital is cancelled, the share capital account is debited and the capital reduction account is debited as share capital is getting reduced.

| Share Capital A/c | Dr. | Amt |

| To Capital Reduction A/c | Cr. | Amt |

When assets and liabilities are revalued

At the time of internal reconstruction, the gain or loss on revaluation is transferred to the capital reduction account instead of the revaluation reserve.

Writing off of accumulated losses and intangible assets

The credit balance of the capital reduction account is used to write off the accumulated losses and intangible assets like goodwill, patents etc which are unrepresented by capital. The capital reduction account is debited and profit and loss account and intangible assets accounts are credited.

| Capital Reduction A/c | Dr. | Amt |

| To Profit and loss A/c | Cr. | Amt |

| To Goodwill/ Patents A/c | Cr. | Amt |

Treatment in books of account

The balance in the capital reduction account, whether debit or credit, it is transferred to the capital reduction account. Hence, it doesn’t appear on the balance sheet.

See less

Introduction Like, in the case of excise duty, the taxable event is the manufacture of goods, supply is a taxable event with respect to the Goods and Services Tax regime in India. A taxable event is an event on occurrence of which tax is charged. Excise duty is charged when any specified good is manRead more

Introduction

Like, in the case of excise duty, the taxable event is the manufacture of goods, supply is a taxable event with respect to the Goods and Services Tax regime in India. A taxable event is an event on occurrence of which tax is charged.

Excise duty is charged when any specified good is manufactured, GST is charged when any good or service is supplied.

Definition of Supply

The concept of supply is of great significance to the GST architecture. It can be called the ‘bones to the body of GST’.

Section 7 of the CGST defines ‘supply’.

At first, I have provided the whole Section 7 which consists of four sub-sections:

Thereafter will be the explanation of each sub-section in simple language.

Section 7

Section 7(1) of the CGST Act, 2017 defines ‘supply’. As per section 7(1) of the CGST Act, 2017, the supply includes:

Section 7(1A) states, ‘where certain activities or transaction constitute as supply in accordance of with the provisions of sub-section (1), they shall be treated either as a supply of good or supply of services as referred to Schedule II.

Section 7(2) states, ‘notwithstanding with anything contained in sub-section (1).

shall not be treated neither as a supply of goods nor a supply of services.

Section 7(3) states ‘subject to sub-section (1), (1A) and (2), the government may, on the recommendation of the council specify, by the notification, the transaction that is treated as :

Explanation of Section 7 in simple terms.

Section 7(1) (a) sets three parameters of an activity or transaction to be a supply.

Any activity or transaction will be treated as a supply if the above parameters are fulfilled as per sub-section (1) clause (a).

Section 7(1)(b) is actually an exception to the 3rd parameter of supply. Import of service for a consideration will be considered a supply even if it is not made in furtherance of business,

Section 7(1)(c) states that item in the schedule I will be treated as supply whether there is consideration or not. This is an exception to the 2nd parameter.

Section 7(1A) states any activity which is a supply as per sub-section (1), shall be classified either as a supply of goods or as a supply of service as per schedule II. There are many activities and transactions which have the characteristics of both goods and services.

For example, dining in a restaurant. Schedule II helps to eliminate this confusion and helps to classify such activities or transactions as either supply of goods or supply of services. As per Schedule II, dining or take-away from a restaurant is a supply of service.

Section 7(2) states the activities which are neither supply of goods nor neither of services even if they fulfilled the condition of the sub-section (1).

Section 7(3) says that the central government have the power to notify transactions that are to be treated as supply of goods nor as a supply of service or supply of services not as a supply of services

See less