Let us begin with a short explanation of what Calls-in-Advance is: Whenever a company accepts money from its shareholders for calls not yet made, then we call it calls-in-advance. To put it in even simpler terms, it is the amount not yet called up by the company but paid by the shareholder. An imporRead more

Let us begin with a short explanation of what Calls-in-Advance is:

Whenever a company accepts money from its shareholders for calls not yet made, then we call it calls-in-advance. To put it in even simpler terms, it is the amount not yet called up by the company but paid by the shareholder. An important thing to note here is that a company can accept calls-in-advance from its shareholders only when authorized by its Articles of Association.

Calls-in-advance is treated as the company’s liability because it has received the money in advance, which has not yet become due. Till the amount becomes due, it will be treated as a current liability of the company.

The journal entry for recording calls-in-advance is as follows:

The money received from the shareholder is an asset for the company and therefore Bank A/c is debited with the amount received as calls-in-advance. The calls-in-advance A/c is credited because it is a liability for the company.

Since Calls-in-Advance is a liability, it is shown in the Equities and Liabilities part of the Balance Sheet under the head Current Liabilities and sub-head Other Current Liabilities.

For better understanding, we will take an example,

ABC Ltd. made the first call of 3 per share on its 10,00,000 equity shares on 1st May. Max, a shareholder, holding 5,000 shares paid the final call amount 2 along with the first call money. Now let me show the journal entry to record calls-in-advance.

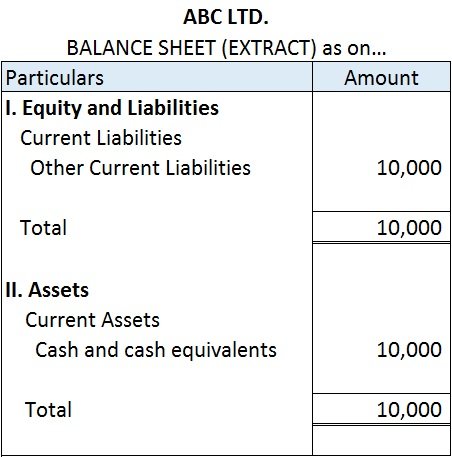

In the Balance Sheet, I will show calls-in-advance in the following manner,

The calls-in-advance of 10,000 is shown under the Equities and Liabilities side of the balance sheet under the head current liabilities and sub-head other current liabilities. It will be shown as a liability till the final call money becomes due. The amount received by the company from Max is shown on the Assets side of the balance sheet under head current assets and under the sub-head cash and cash equivalents.

See less

A profit and loss account is a financial statement which shows the net profit or net loss of an enterprise for an accounting period. It reports all the indirect expenses and indirect income including gross profit or loss derived from trading accounts for an accounting period. When the total revenueRead more

A profit and loss account is a financial statement which shows the net profit or net loss of an enterprise for an accounting period. It reports all the indirect expenses and indirect income including gross profit or loss derived from trading accounts for an accounting period.

When the total revenue i.e. credit side of profit and loss a/c is more than the total of expenses i.e. the debit side of profit and loss a/c, it results in net profit whereas when the total revenue is less than the total of expenses, it results in a net loss.

The debit balance of the profit and loss account is the net loss incurred during the accounting period by an enterprise. It is transferred to a capital account thereby reducing the capital or can be shown as a debit balance on the asset side.

Accounting entry for loss transferred is as follows :

Capital A/c …Dr.

To Profit & Loss A/c

(being net loss transferred to capital account)

Example

A Business has a total income of $50,000 in an accounting year and has expenses amounting to $60,000 in that particular year. The profit and loss account will show a net loss of $10,000 ($60,000-50,000). Net loss will be transferred to capital A/c. Capital of the business will be reduced by $10,000. This loss can also be shown on the asset side of the balance sheet.

Extract of a Profit and loss a/c showing net loss is as under:

Profit and loss A/c for the year ended …..

The debit balance for a non-corporate entity is shown as a reduction from the capital account

Extract of the Balance sheet showing the debit balance of Profit & Loss A/c is as under :

Balance Sheet as on…

Less: Profit & Loss A/c

While the Debit balance of profit and Loss A/c of a corporate entity is shown as a reduction in Reserves and surplus. If the business doesn’t have reserves then the debit balance is shown on the asset side.

Extract of the Balance sheet showing the debit balance of Profit & Loss A/c is as under :

Balance Sheet as on..

Less: Profit & Loss A/c

Conclusion: Debit balance of profit and loss a/c represents that expenses are more than the income of a business in an accounting period. Debit balance of profit and loss a/c indicates that company need to increase its income or cut down on unnecessary expenses.

The business needs to find out the reason of excessive expenses because accumulated losses are not good for the health of the company.

See less