1) Liability 2) Asset 3) Expenses 4) Income

1) A simple petty cash book is like a cash book. Definition The term 'petty' means small. A simple petty cash book is identical to a cash book, maintained to record the small expenses of a business like stationery, postage, stamps, carriage, etc. The cash received by a petty cashier is recordRead more

1) A simple petty cash book is like a cash book.

Definition

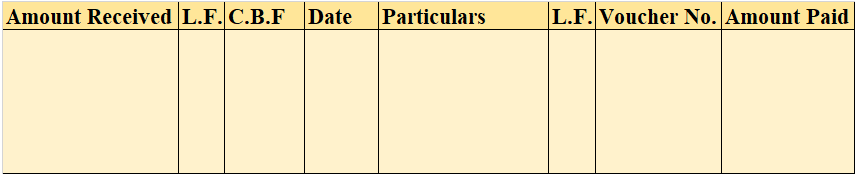

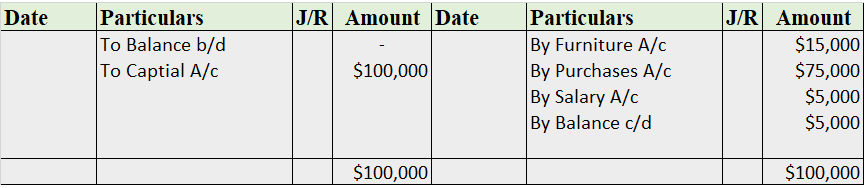

The term ‘petty’ means small. A simple petty cash book is identical to a cash book, maintained to record the small expenses of a business like stationery, postage, stamps, carriage, etc. The cash received by a petty cashier is recorded on the debit/ receipt side whereas, the cash he pays is recorded on the credit/ payment side. The difference between the sum of the debit and credit items represents the balance of the petty cash in hand.

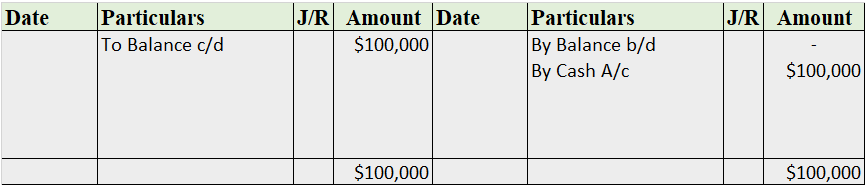

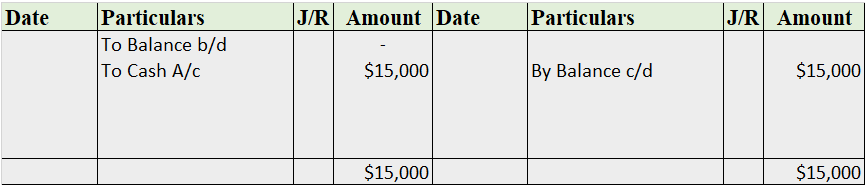

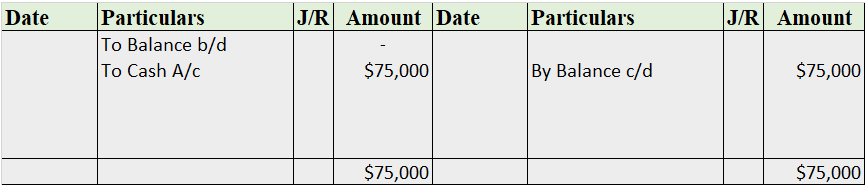

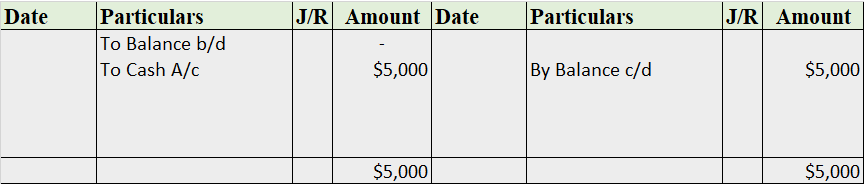

Format

Explanation

Cash Book – A simple petty cash book is recorded and maintained just like the cash book. Just like a cash book records all the major transactions of the business, a petty cash book only focuses on the expenses which are of little value. Just like the cash book is maintained by the accountant of the business, the petty cash book is maintained by the petty cashier.

Therefore, a petty cash book is like a sub-part of a cash book itself.

Statement – A statement in accounting terms refer to a report. They are prepared to show some accounting data and different types of statements show different perspectives of the company’s financial health and performance. For e.g Balance sheet, trial balance, cash flow statements, etc.

Thus, a petty cash book is not a part of statements in accounting.

Journal – A petty cash book is not a part of a journal as a journal entry records business transactions in the accounting system for an organization and is also called the building block of the double-entry accounting method. While a petty cash book is maintained to record the small expenses of a business that are of little value.

Therefore, 1) Cash book is the correct option.

See less

Therefore, 2) Asset is the correct option. Explanation The petty cash book is managed and made by not an accountant but the petty cashier and is done to record small incomes and expenditures that are not recordable in the cash book. Therefore, the desired result we obtain from the deduction oRead more

Therefore, 2) Asset is the correct option.

Explanation

The petty cash book is managed and made by not an accountant but the petty cashier and is done to record small incomes and expenditures that are not recordable in the cash book. Therefore, the desired result we obtain from the deduction of the total expenditure and total cash receipt is the closing balance of the petty cash book.

Petty cash refers to the in-hand physical cash that a business holds to pay for small and unplanned expenses.

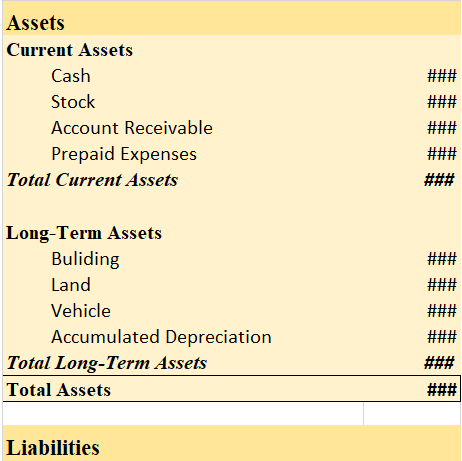

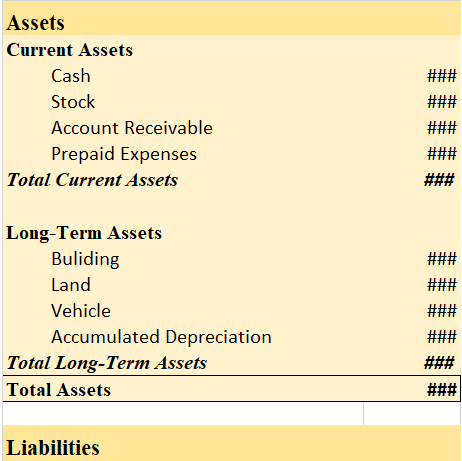

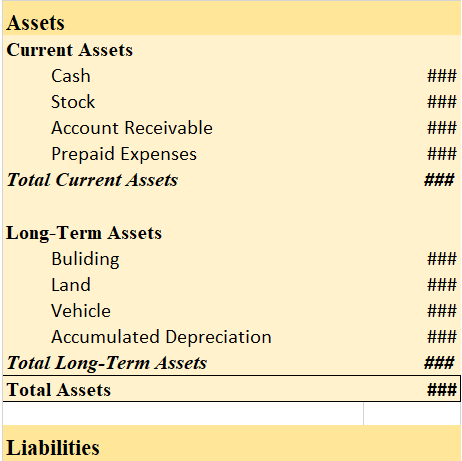

Asset: The closing balance of the petty cash book is considered an asset because the petty cash book is a type of cash book. The petty cash book also deals in outflow and inflow of the cash, it also maintains and records income and expenditure that are similar to the cash book.

The petty cash book since being a part of the cash book, which records all the inflow and outflow of cash in a business, which is an asset, thus petty cash book’s closing balance is considered an asset. Also, the balance of the petty cash book is never closed. Their closing balance is carried forward to the next year.

Liability: The closing balance of the petty cash book is not considered a liability because that closing balance of the petty cash book doesn’t create a liability for the business. In fact, the closing of the petty cash book is placed under the head current asset in the balance sheet as mentioned above, it’s a part of the cash book which records the transactions of cash a/c which is an asset itself.

Expenses or Income: It is not an expense because the closing balance of the petty cash book is calculated by deducting the total expenditure from the total cash receipt.

That is an asset and it is considered to be a current asset, neither an income nor an expense. It is used for paying out petty expenses.

Therefore, the closing balance of the petty cash book is considered an asset.

See less