A contra account is a general ledger account that is used to reduce the value of the account related to it. Basically, a contra account is the opposite of its associated account. If the associated account has a debit balance, then the contra account would have a credit balance. They are used to mainRead more

A contra account is a general ledger account that is used to reduce the value of the account related to it. Basically, a contra account is the opposite of its associated account. If the associated account has a debit balance, then the contra account would have a credit balance. They are used to maintain the historical value of the main account while all the deductions are recorded in the contra account, which when clubbed together show the net book value.

For example

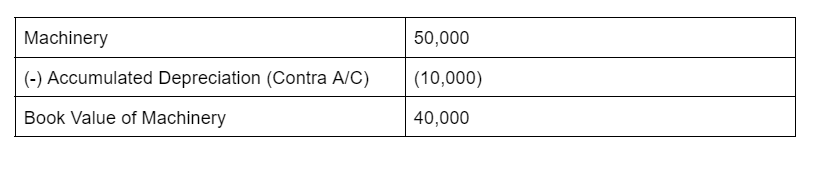

if the cost of machinery was Rs. 50,000 and the company wants to preserve its original cost, then the accumulated depreciation of such machinery is recorded separately. Let’s say Rs 10,000 was the accumulated depreciation. Then such amount is recorded in the contra account named accumulated depreciation account. This makes the net value of the machinery Rs 40,000.

Types

There are various types of contra accounts such as contra asset, contra equity, contra revenue, and contra liability.

- Contra asset: these accounts have credit balances and are used to reduce the balance of an asset. Eg, Accumulated depreciation.

- Contra Liability: These accounts have debit balances and are used to reduce the balance of liabilities. Eg, discount on notes.

- Contra equity: These accounts have a credit balance and are used to reduce the number of shares outstanding which in turn reduces equity. Eg treasury stock.

- Contra revenue: These accounts have a debit balance. They reduce gross revenue which results in net revenue. Eg sales return.

Accountants make use of contra accounts instead of reducing the value of the actual account to keep the financial statements clean.

See less

The debts that have a higher chance of not being paid are called doubtful debts. They are a part of the regular dealing of the company and may arise due to disputes or treachery on the part of debtors. Bad debts refer to the doubtful debts that no longer seem to be recoverable from the business. WriRead more

The debts that have a higher chance of not being paid are called doubtful debts. They are a part of the regular dealing of the company and may arise due to disputes or treachery on the part of debtors.

Bad debts refer to the doubtful debts that no longer seem to be recoverable from the business.

Written off means an expense, income, asset, liability is no more recorded in the books of accounts because they no longer hold relevance for the business.

When doubtful debts turn into bad debt, they are written off from the books after a stipulated time as they no longer seem recoverable.

If any cash is received against such bad debts that were written off, it is known as cash received against bad debts written off. Cash is received against bad debts usually when the debtor is declared insolvent and money is recovered from its estate.

Bad debts recovered are considered an income for the company as they were previously written off as a loss and any cash received against it is considered as income.

Journal entry for such situation is:

Cash or Bank A/c (Dr.)

To Bad Debts Recovered A/c

We debit the increase in assets, and since cash is coming into the business it is debited.

We credit the income, and since bad debts recovered is an income to the business it is credited.

See less