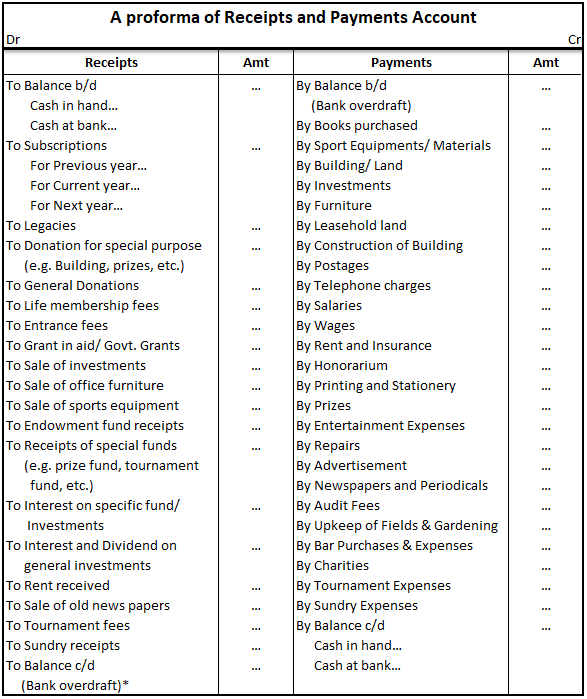

1) A simple petty cash book is like a cash book. Definition The term 'petty' means small. A simple petty cash book is identical to a cash book, maintained to record the small expenses of a business like stationery, postage, stamps, carriage, etc. The cash received by a petty cashier is recordRead more

1) A simple petty cash book is like a cash book.

Definition

The term ‘petty’ means small. A simple petty cash book is identical to a cash book, maintained to record the small expenses of a business like stationery, postage, stamps, carriage, etc. The cash received by a petty cashier is recorded on the debit/ receipt side whereas, the cash he pays is recorded on the credit/ payment side. The difference between the sum of the debit and credit items represents the balance of the petty cash in hand.

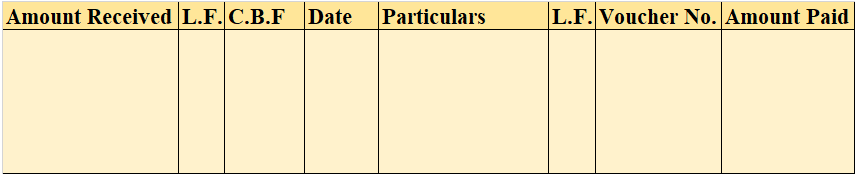

Format

Explanation

Cash Book – A simple petty cash book is recorded and maintained just like the cash book. Just like a cash book records all the major transactions of the business, a petty cash book only focuses on the expenses which are of little value. Just like the cash book is maintained by the accountant of the business, the petty cash book is maintained by the petty cashier.

Therefore, a petty cash book is like a sub-part of a cash book itself.

Statement – A statement in accounting terms refer to a report. They are prepared to show some accounting data and different types of statements show different perspectives of the company’s financial health and performance. For e.g Balance sheet, trial balance, cash flow statements, etc.

Thus, a petty cash book is not a part of statements in accounting.

Journal – A petty cash book is not a part of a journal as a journal entry records business transactions in the accounting system for an organization and is also called the building block of the double-entry accounting method. While a petty cash book is maintained to record the small expenses of a business that are of little value.

Therefore, 1) Cash book is the correct option.

See less

Return inwards are the goods returned by the customer to the seller. The goods are returned for reasons like defects, excess delivery, and low quality. Return inwards are also known as Sales Returns. Sales returns are a contra account to sales revenue. The amount of sales returns is deducted from thRead more

Return inwards are the goods returned by the customer to the seller. The goods are returned for reasons like defects, excess delivery, and low quality. Return inwards are also known as Sales Returns.

Sales returns are a contra account to sales revenue. The amount of sales returns is deducted from the total sales in the Trading section of the Trading and Profit & Loss Account.

In subsidiary books, return inwards are recorded only for those goods which are sold on credit to the customer.

For example, On 1 August E Electronics sold 50 units of television to Hill Hotels on credit for Rs.25,000 each. Out of which 5 units were found to be defective and were returned back to E Electronics. In that accounting period, E Electronics made a total sales of Rs.20,00,000 (including the item sold to Hill Hotels).

E Electronics in its Trading section of Trading and P&L A/c will account for a sales return of Rs.1,25,000 (Rs.25,000*5) and this amount will be deducted from the total sales. The same will be recorded in the subsidiary books as it accounts for sales made on credit.

Extract of Profit & Loss Account:

For a business, sales returns will either have a decrease in the sales revenue or it will increase the sales returns and allowances which is a contra account to sales revenue. An increase in sales returns will decrease gross profit.

See less